About the Company

Incorporated in 2006, Barbeque Nation is one of the leading casual dining chains in India. Barbeque Nation Hospitality Limited (BNHL) is a pioneer in “over the table barbeque” live grills embedded in dining tables. Having a significant presence in India’s hospitality sector, Barbeque Nation is one of the most visited and widely recognised restaurant brands in the rapidly growing casual dining restaurant market of India. As on 31st March 2020, BNHL had a chain of 150 restaurants across 77 cities and towns in India. It is operating 6 restaurants in International markets of Middle east and Malaysia.

Q3 FY23 Update

Financial Results & Highlights

Detailed Results:

- There was a marginal decline in same store sales growth by 1.2%.

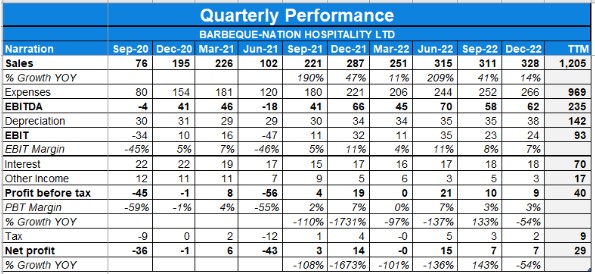

- In Q3 FY2023 consolidated revenue from operations were Rs.328.2 Crores, delivering a year-on-year growth of 14.5% and sequential growth of 5.7%.

- Dine in business grew by 4.4% led by volume growth. Delivery business has seen a growth of 15% on sequential basis entirely led by volume growth.

- Gross margins improved by 60 basis points.

- EBITDA margin for the quarter was Rs. 63 Crores.

- EBITDA margin was 19.2% as compared to reported EBITDA margins of 24.5% in the same quarter of the previous year.

- Consolidated gross margin for the quarter was 66.7% compared to 66.1% in Q2 in FY2023.

- The new restaurants reported margins of 5.3% with average annualized revenue of around Rs.4.5 Crores.

- Revenue from Toscano business increased by around 45%

- International business recorded year-on-year revenue growth of around 23% with very strong margins.

- Nine-month capex is approximately Rs.110 Crores that the company has incurred.

Investor Conference Call Highlights

- The management stated that of the existing 212 restaurants, Barbeque Nation India network has 192 restaurants, Toscano has 14 restaurants and international portfolio has six restaurants.

- The management stated that currently around 14 restaurants are under construction and they are confident of achieving their target of 40 new restaurants during FY2023.

- The management stated that the growth in revenue from operation was led by 18% growth in dine-in business driven by both increase in dine-in volumes and prices.

- The management stated that their margins were impacted by a higher mix of new and yet mature restaurants coupled with lower than expected SSSG growth of the matured portfolio.

- The management stated that on a year-to-year basis, their delivery segment has declined by 3% led again by decline in average order value which was offset by increasing number of transactions in the delivery segment.

- The management stated that Dum Safar, their new Biryani brand is now available at over 50% of their network and it continues to generate strong traction with customers.

- The company’s SSSG in the core dine-in segment was positive 1.7%. While SSSG in the delivery segment, it was negative.

- The management stated that the improvement in gross margin was driven by operating efficiencies and stable input cost.

- The management stated that of the total 5.1% decline in margins, approximately 190 basis points (bps) was due to lower SSSG and impact of negative operating leverage and around 220 bps was impacted due to change in revenue mix between matured and new stores.

- The management stated that Overall app downloads have increased to around 5.4 million.

- The share of Barbeque Nation India revenues from its own digital assets was 27.6% in Q3 FY2023.

- The management stated that for the new stores, in the first six months it was almost break even post that end of year one, it reached to around 7% to 8%. At the end of say year two it will be around 15% and the year three it reaches to around 20% to 21%.

- The management stated the reason for the closure of the three stores. Two of them were shut down because the company did not see that expansion in margins and the biggest issue was the management bandwidth that it used to take. Another store was shut down because the location of that particular site was an issue.

- The management stated that the restaurants in tier three cities have not done that great.

- Out of 40 sites that the company opened this year around 37 of these are from Barbeque Nation, three are coming from Toscano and none from international.

- The management stated that the month on month ADS on the bucket of Dum Safar is approximately Rs. 7,000 now. This is per day right so they think on all fronts they are seeing some traction on this business.

- The management told the distribution of the capex which is divided in broadly three categories. So, approximately Rs.90 Crores has gone into new restaurants, around Rs.10 Crores have gone into regular maintenance capex and another Rs.10 Crores have gone into two of their specialized projects one is Biryani brand Dum Safar and other in water projects that they have taken up this year.

- The management stated that they hosted some campaigns to target specific customer groups and specific day parts to increase the attraction like Happy Monday and Tuesday offers etc.

Analyst’s View

Barbeque Nation is one of the most recognizable casual dining restaurant chains in India.The company is confident of achieving their target of 40 new restaurants during FY2023. The company has also gained traction on its digital platform. It remains to be seen what obstacles will the company face in expanding the new restaurant chain, generate meaningful SSSG to ensure operating leverage kicks in & margins are maintained and whether it will be able to scale up its delivery business in competition to 3rd party delivery majors like Dominos, Swiggy and Zomato. With the reduction in the total debt, the annual interest and repayment obligation has reduced considerably, leading to the availability of internal accruals for opening new outlets. Nonetheless, given the good brand recall, wide geographical reach and the vast potential of the Indian Food Services sector, Barbeque Nation is an interesting stock to watch out for.

Q2 FY23 Update

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 274 | 206 | 33.33% | 278 | -1.55% | 761 | 453 | 67.99% |

| PBT | 8 | 5 | 65.96% | 16 | -50.00% | 36 | -90 | – |

| PAT | 6 | 4 | 59.55% | 11 | -50.39% | -22 | -70 | – |

| Consolidated Financials (in Crs) | ||||||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 312 | 229 | 36.07% | 318 | -1.83% | 861 | 507 | 69.82% |

| PBT | 10 | 4 | 134.88% | 21 | -51.44% | -32 | -112 | – |

| PAT | 8 | 3 | 125.45% | 16 | -52.94% | -26 | -90 | – |

Detailed Results:

- The company had a good quarter with revenue growth of 36% and profits growth of 125% YoY on the consolidated basis.

- QoQ performance looks muted, with revenue and profits falling by 2% and 53% respectively.

- Added 10 new stores during the quarter taking the total store count to 205 stores. Out of these 10 restaurants, 7 were added in metro and Tier 1 markets and 3 were added in Tier 2 cities.

- Of 205, Barbeque Nation India network has 186 restaurants, Toscano has 13 restaurants and the international portfolio includes 6 restaurants.

- Same-store sales growth of 23.4%.

- Dine-in business has grown by 61% on a year-on-year basis. Dine-in business growth was partially offset by a 23% year-on-year decline in delivery revenues.

- Gross margins improved by over 40 basis points during the quarter as compared to the previous year and dropped by 70 basis points as compared to the previous quarter

- The reported EBITDA margin was 19.3% as compared to the reported EBITDA margin of 22.6% in the same quarter of the previous year. Core EBITDA growth of 39.1% versus the previous year.

- The share of box business has declined and the share of a-la-carte orders have increased

- Barbeque India’s revenue grew year-on-year by 38%. Revenue from Toscano’s business doubled compared to the same period last year. And international business recorded year-on-year revenue growth of 28%.

- The consolidated gross margin for the quarter was 66.1% compared to 65.6% in Q2 FY22.

- On a sequential basis, gross margin declined by 70 bps, largely led by input cost inflation.

- Net cash flow from operating activities of INR 135 crores during first half of this fiscal year.

- Overall app downloads increased to around 5.1 million and the share of Barbeque Nation India revenue from its own digital assets has gone to around 28.7% in Q2 FY23.

- In H1 basis, international businesses at a corporate level delivered 18% pre-Ind AS margin.

Investor Conference Call Highlights

- The management remains confident of achieving the guidance of 40 stores for FY23, this should include 33 to 35 Barbeque Nation restaurants in India, around 4 to 5 Toscano restaurants, and 1 to 2 Barbeque Nation in the international business, again, primarily the Middle East.

- The company has around 16 restaurants under construction and an equally strong pipeline of sites under evaluation.

- While delivery business volumes have increased on a year-on-year basis, average order values (AOV) have come down due to the change in product mix.

- The management stated the Biryani brand ‘Dum Safar’ was launched during the second half of the quarter across 25 locations. The initial response to this product has been very encouraging and the company plans to launch Dum Safar across all restaurants in a phased manner by the end of FY23. As on September, it is in around 25 outlets. As on October, in around 42 outlets. By end of December, the company will try and go to around 75 and try to be in all the outlets by end of this financial year.

- The management are seeing a moderation in some of the input costs and believe that the gross margins should marginally expand during the second half of the year.

- The management stated after a few quarters of sequential decline in delivery, they are seeing an uptick in overall daily delivery sales and believe that going forward, the delivery business would start contributing to overall growth.

- The company has also not taken any structural price hikes during the quarter, which improved operating efficiencies and enabled the company to manage gross margins better.

- As the company enters a seasonally stronger second half of the business, the management remains confident of delivering the average annualized revenue of INR 7 crores per restaurant with around 21% restaurant operating margin in a mature portfolio. The drag should not be more than 1% point.

- The matured portfolio delivered 6.67 crore revenue per store with an operating margin of 19.2% in Q2.

- The management stated for the 40 restaurants that the company is opening up, CAPEX for maintenance, and some towards the Biryani project, there will be approximately INR 135 crores of CAPEX in this financial year. And based on the growth plan for next year and assuming that it remains at between say, 40 to 45 restaurants next year also, the CAPEX would be anywhere between INR 135 to INR 150 crore.

- The management stated in long term, the company will be at an AOV of between INR 500 to 550 and then focus on growing the transaction volumes in the delivery business.

- The management stated original INR 50 crores to INR 55 crores per quarter run rate on delivery is achievable from Q1FY24.

- The management stated almost 25% of the company’s portfolio is less than one year old. That too in a seasonally weaker quarter and also the portfolio is more skewed towards metro markets, where the initial losses are slightly more than Tier 2 / Tier 3 sites. And that’s why once this portfolio of 40 restaurants sort of goes through their initial cycle of two years, this will start delivering the same return as the mature portfolio.

- The management stated for the new store, 0 to 6 months typically flattish or very low single-digit margins. For the entire first year, they would look at around 7% to 8% margins. Second year, they look at store margins of around 14%-15% and third year it will come to around 21%.

- In value terms one box business is equal to 1.5 a-la-carte order.

- Menu re-engineering, delivery rating, and managing delivery from the same restaurant in an efficient manner are the kind of strengths that the company building around delivery business.

- The management stated between last year, the second quarter, and this second quarter, pricing would have gone up by around 7- 8%. This quarter, the company has not taken any price hikes. Did around 4.5% price hike in Q1. The company is not planning to do any incremental price hikes in the second half.

- The management stated festive season is not really good for them as their major business is non-veg, hence October was leaner for them, and they expect the kick-in demand in December.

- On the meat front, the management stated there’s one commodity, which is fish, which is largely imported. That pricing was higher in Q2 as compared to Q1. Also across other businesses, for example, International business, gross margin was down by around 1.5%. In Middle East business, largely most of the items are imported, and there were some input cost hikes. Similarly, in the Toscano business, there was some marginal increase in the cost. So the gross margin declined between, Q1 and Q2, across all three verticals. The impact was lowest for Barbeque India and pretty much highest for international. The new shipment that the company got in the month of September is at lower pricing. So that gives some confidence in the H2 margin.

- The company has only opened two stores of Toscano this year. And they hope to do two more. One is under construction and one more will go in the construction in the next few days.

- The management stated in terms of stores opening for International business, the company is only doing it from the profit that it is getting from that business. So this year may be one happening and maybe two more in the subsequent year.

- Comparing revenue from the dine-in business pre-COVID same quarter, on the same matured portfolio, it is pretty much the same today. It’s flat. So price hikes have offset some of the lower footfalls.

- Rent paid in Q2 is 62 crores, 10% of the topline.

- The management stated pricing in some of the markets like Bombay Delhi, Bangalore, is different than what the company charge in some of the other locations. Pricing can be different within the same city also.

- Same-store sales growth of around 5-7% CAGR over three years, with almost two years of COVID, around 10% of this came from delivery and the balance came from the pricing.

- The management’s hope is that volumes will come back as IT further opens up and our corporate business moves up.

- The management stated when they launched it in late 2018, the business was contributing hardly INR 40 lakhs per month. And they are excited about that business being approximately INR 200 crores, soon.

- On the cloud kitchen front, the management stated first, they have to fix the ADS growth in our existing outlet and bring it to a point that it at least does not bleed money in extension kitchens. Once it’s reached that point, adding cloud kitchens is not a big problem for. These are 600 sq. feet of outlets this can be done quickly. And that they will do once delivery ADS sort of comes back.

- The management stated in a normal year, the Q3 ADS is 12-15% higher compared to the Q2 ADS in terms of total sales. Per store basis, this should be around 10% higher.

Analyst’s View

Barbeque Nation is one of the most recognizable casual dining restaurant chains in India. The company has done well to get back the dine-in sales to above pre-covid levels and to ramp up its delivery business which has seen 5.1 million cumulative downloads. The company has opened up 10 new units in Q2FY23 and 21 in H1 so far and 40 more are on the roadmap for this year. It remains to be seen what obstacles will the company face in expanding the new restaurant chain and whether it will be able to scale up its delivery business in competition to 3rd party delivery majors like Dominos, Swiggy and Zomato. With the reduction in the total debt, the annual interest and repayment obligation has reduced considerably, leading to the availability of internal accruals for opening new outlets. Nonetheless, given the good brand recall, wide geographical reach and the vast potential of the Indian Food Services sector, Barbeque Nation is an interesting stock to watch out for.

Q1 FY23 Update

Financial Results & Highlights

| Standalone financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY21 | FY22 | YoY% | |

| Sales | 276 | 86 | 220% | 223 | % | 453 | 761 | 68% |

| PBT | 16 | -48 | – | -3 | % | -90 | 36 | – |

| PAT | 11 | -36 | – | -2 | % | -70 | -22 | – |

| Consolidated financials (in Crs) | ||||||||

| Q1FY23 | Q1FY22 | YoY % | Q4FY22 | QoQ % | FY21 | FY22 | YoY% | |

| Sales | 315 | 102 | 308% | 257 | 22.5% | 507 | 861 | 70% |

| PBT | 21 | -24 | – | 2 | 105% | -112 | -32 | – |

| PAT | 15 | -38 | – | 0.4 | 3750% | -90 | -26 | – |

Detailed Results

- Company’s consolidated quarterly revenues crossed Rs. 300 Crores for the first time in the history of Barbeque Nation, which is around 3x of previous year Q1.

- Net cash of Rs 66 crores.

- The company reported a healthy EBITDA margin of 23.3%.

- On a sequential quarter basis, the company grew 25.4% driven by growth in volume and average realization.

- Company reported strong SSSG year-on-year of 182% as compared to the previous quarter of 19.8%.

- Barbeque Nation’s dine-in to delivery mix changed in favor of dine-in. Dine-in segment has grown around 6x versus the previous year and 32% versus the previous quarter.

- Company reported a gross margin of 66.8%.

- Company reported an EBITDA of Rs. 73.4 Crores in 1QFY2023 delivering a healthy margin of 23.3% while adjusted EBITDA was Rs 46 Crores, delivering 14.6% margin.

- Incremental capex of around Rs 37 Crores have been done- Rs 3 Crores on maintenance capex and around Rs 34 Crores on new sites. Rs 3 Crores is the net increase in cash balance.

Investor Conference Call Highlights

- Highest Revenue was driven by targeted efficiency projects, better cost management, calibrated price increase and change in business mix towards dine-in.

- The company wants to build one of India’s largest food service companies owning its restaurant brands.

- Company has added nine new restaurants taking the total India network to 176 number of restaurants.

- Management commented that their India business is growing by higher covers and higher realization per cover.

- Management plans to cross 200 outlets of Barbeque Nation in India in this financial year.

- International business is the highest margin business in our portfolio with store margins of over 25% plus, looking to add 2-3 restaurants this year.

- Toscano business has grown by around 54% versus the previous quarter and plan is to add around five more restaurants this year. Toscano delivered healthy store margins of 23% plus in this quarter.

- Total 195 restaurants as on June 30, 2022, around 80% restaurants are matured i.e. more than two years old. This matured portfolio delivered annualized sales of around Rs. 7 Crores per outlet with store margins of 21.5%.

- Company has a robust under-construction pipeline and a strong pipeline of work-in-progress sites and is progressing well towards its target of 40 restaurants in FY2023.

- Q2 is unfortunately the weakest quarter, this has Shravan, Shradh, even Durga Puja, Navratri, all in this quarter, this is actually not good for nonveg consumption in India and that impacts us definitely. The best quarter for company is Q3 followed by Q4, Q1 and then Q2.

- Barbeque Nation is actually working on a dedicated delivery only online biryani brand. This is at a stage wherein this month company should pilot it in a few locations and depending on the success there will take it up pan India.

- Management is exploring franchising in few of the geographies, but the lead timing one these are really very high.

- Most of the IT corporates also are not fully back. So, weekday lunch business is still slightly lower than what company used to do on a pre-COVID basis. Apart from that, on the weekend side or on the friends and family segment side, management believes they are pretty much sorted here.

- Company is planning to add up to 300 outlets in the next couple of years.

- Management guided that they want to make delivery as at least 20% of your overall business. The focus first is to increase average daily sales from the existing network which is now close to 195, once this goes up and individually this can sustain in extension kitchen also then adding more extension kitchen is not a problem.

- Management believes capex of around Rs.130 Crores to Rs.140 Crores for stores addition.

- Employee attrition rate higher than the usual numbers during the COVID times, a lot of international hires, cruise lines etc. were not hiring – those avenues have opened up for a lot of people.

- Company has taken around 4% to 5% price hike in the current quarter, which was actually taken in the month of April and May spread across the two months.

- Management believes the inflation trends on COGS won’t put any significant risk to gross margins.

Analyst’s Views

Barbeque Nation is one of the most recognizable casual dining restaurant chains in India. The company has done well to get back the dine-in sales to above pre-covid levels and to ramp up its delivery business which has seen 4.7 million cumulative downloads. The company has opened up 9 new units in Q1FY23 so far and 40 more are on the roadmap for this year. It remains to be seen what obstacles will the company face in expanding the new restaurant chain and whether it will be able to scale up its delivery business in competition to 3rd party delivery majors like Dominos, Swiggy and Zomato. With the reduction in the total debt, the annual interest and repayment obligation has reduced considerably, leading to the availability of internal accruals for opening new outlets. Nonetheless, given the good brand recall, wide geographical reach and the vast potential of the Indian Food Services sector, Barbeque Nation is an interesting stock to watch out for.

Q4 FY22 Update

Financial Results & Highlights

| Standalone financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 632 | 615 | 2.8% | 557 | 13.5% | 2346 | 2163 | 8.5% |

| PBT | 98 | 130 | -24.6% | 42 | 133.3% | 335 | 391 | -14.3% |

| PAT | 94 | 140 | -32.9% | 30 | 213.3% | 252 | 315 | -20.0% |

| Consolidated financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 257 | 237 | 8.4% | 291 | -11.7% | 887 | 553 | 60.4% |

| PBT | 2 | 8 | -75.0% | 19 | -89.5% | -32 | -111 | -71.2% |

| PAT | 0.4 | 6.4 | -93.8% | 15 | -97.3% | -25 | -92 | -72.8% |

Detailed Results

- The company reported a revenue growth of close to 10% YoY in Q4FY22.

- EBITDA decreased by 10% while margins stood at 20.1%.

- Delivery revenue increased by 56.5% YoY

- Restaurant operating margins for the quarter stood at 14.4%.

- Total restaurant count as on April 2022 stood at 185 which included 168 BBQ indian stores, 6 BBQ international & 11 italian restaurants under the brand TOSCANO.

- The company also has 15 extension kitchens as on April 22.

- Dine-in recovery was 110% of pre-covid period of Q4 FY21.

- Delivery segment was 18% of the total revenue from operations in Q4 FY22

- Cumulative BBQ App downloads stood at 4.2mn+, which is a 63% increase over March’21.

- Channel contribution was at 24.1% of its own app.

- The loyalty program SMILES saw 16.7% share of total bills in Q4 2022.

Investor Conference Call Highlights

- The management states that the company is confident of growing its restaurant strength by 35 to 40 restaurants in FY 23.

- The company is targeting a restaurant count of 300 by FY25.

- The management doesn’t expect capex per store to increase despite inflation.

- The company expects to open 3-4 stores every month from the current quarter.

- The management clarified that RBL bank sold the pledged shares of the company because they wanted to come out of the association & management further states that banks now have zero pledged shares with them.

- The company expects the delivery biz to grow at 20% CAGR over the next few years.

- The company didn’t take a price hike in Q4 as the priority was on growing volumes due to the Omicron wave. However, the company has now taken a price hike of 5% between April & May which will help in tackling inflation.

- The company aspires to increase gross margins from 65-66% to 67-68% in the next 3-4 years.

- The management states that due to its strong analysis & menu reengineering strategy, it has been able to maintain decent gross margins despite input cost inflation.

- The margins for the current quarter got squeezed also due to high fixed costs in the form of high inflation in employee costs coupled with rental costs. However, the company expects to reach 20% margins at the portfolio level in Q1FY23.

- The management expects rental costs per store to stay at around 10-10.5% of revenues.

- The company’s revenue framework & seasonality leads to sales break-up of 45-47% from H1 & around 53% from H2.

- The management is planning to increase the store count of TOSCANO from 11 stores to 16-17 stores by the end of FY23.

- The company on a normalized basis expects store revenue of Rs.7 Cr which includes delivery sales.

- The company’s top 20 restaurants, which is approximately 12% of its total restaurant network contribute between 18% – 20% of the entire revenue.

Analyst’s Views

Barbeque Nation is one of the most recognizable casual dining restaurant chains in India. The company has done well to get back the dine-in sales to above pre-covid levels and to ramp up its delivery business which has seen 4.2 million cumulative downloads. The company has opened up 12 new units in Q4FY22 so far and 14 more are in the construction phase. Its Italian restaurant chain Toscano is also expected to open new stores and reach 20-25 stores in the next 2 years. It remains to be seen what obstacles will the company face in expanding the new restaurant chain and whether it will be able to scale up its delivery business in competition to 3rd party delivery majors like Dominos, Swiggy and Zomato. Nonetheless, given the good brand recall, wide geographical reach and the vast potential of the Indian Food Services sector, Barbeque Nation is an interesting stock to watch out for.

Q3 FY22 Update

Financial Results & Highlights

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 291 | 203 | 43.3% | 229 | 27.1% | 630 | 316 | 99.4% |

| PBT | 19 | -3 | 733.3% | 4 | 375.0% | -33 | -122 | 73.0% |

| PAT | 15 | -1 | 1600.0% | 3 | 400.0% | -26 | -98 | 73.5% |

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 260 | 182 | 42.9% | 205 | 26.8% | 559 | 280 | 99.6% |

| PBT | 18 | -1 | 1900.0% | 4 | 350.0% | -25 | -100 | 75.0% |

| PAT | 14 | 0.6 | 2233.3% | 3.5 | 300.0% | -19 | -77 | 75.3% |

Detailed Results

- The company reported strong revenue growth of 47% YoY

- EBITDA increased by 41% while margins stood at 24.5%.

- Delivery revenue increased by 64% YoY

- Restaurant operating margins for the quarter stood at 20.7%.

- Total restaurant count as on Jan 2022 stood at 177 which included 160 BBQ indian stores, 6 BBQ international & 11 italian restaurants under the brand TOSCANO.

- The company also has 12 extension kitchens as on Jan 22.

- Dine-in recovery was 108% of pre-covid period of Q3 FY20

- Delivery segment was 16% of the total revenue from operations in Q3 FY22

- Cumulative BBQ App downloads stood at 3.6mn+, which is a 63% increase over Dec’20.

- Channel contribution was at 25.6% of its own app, 53.9% from the non-digital reservation and walkin, & 20.5% from 3rd party digital apps.

- The loyalty program SMILES saw 14.5% share of total bills in Dec 2021.

Investor Conference Call Highlights

- Due to Q3 being the first quarter with minimal restrictions, company delivered its highest ever quarterly sales and EBITDA

- The management states that due to input price inflation especially in the prices of meat, prawn etc, the company has taken price hikes at portfolio level of roughly 5-6%.

- The company plans to close the delivery sales for the year at Rs.200 Cr and then further grow this segment at 20-25% in the coming years and this business is expected to contribute 15-20% of total revenues of the co.

- The company’s majority of delivery sales comes from its offering ‘barbeque in box’ which has 1.8-2 times APC in comparison to industry standards leading to better economy of its delivery offerings.

- The company’s delivery business has been stable despite pick up in dine in activities.

- The management doesn’t expect any further price hikes in its business. Further due to maturing of the delivery business, the food cost is reducing leading to better margins.

- The company generated operating cash flow of Rs.45 Cr with debt being at Rs.20 Cr and cash balance being Rs.115 Cr.

- Due to extension kitchens, the per store sales have reduced by 4-5%

- The management expects to add 10-12 new stores in the coming quarter

- The management says that it will be able to maintain its gross margins. It also said that due to opening up of corporates and cities in general, dine-in contribution will increase leading to the company delivering 15% EBITDA in the coming year.

- The management believes that the Italian food subsidiary Toscano will do better in the coming time and is guiding for growth of outlets from 13 to 20-25 within the next 2 years.

- The company is guiding to reduce the gap between restaurant & company margins to 5% in the coming quarters.

- The management took steps to reduce employee expenses by reducing no. Of employees during covid by 10% and also rationalizing the employee mix.

- Larger number of its stores operate on the fixed rental model currently.

- The company had poor experience in the past in its international business however currently it is very bullish on its international business as it is clocking 20% EBITDA & SSSG of 35% & the payback period is similar to that of indian business

- The company has a policy where it pays approximately 4% service charge to its employees, so that they feel part of the growth story of the company thus as sales increase the employee expenses also increases although at lower proportion.

- The company spends only 1-1.5% of revenues on advertisement expense as it is more focused on word of mouth advertising

Analyst’s Views

Barbeque Nation is one of the most recognizable casual dining restaurant chains in India. The company has done well to get back its dine-in sales above pre-covid levels and to ramp up its delivery business which has seen 3.6 million cumulative downloads. The company has opened up 14 new units in FY22 so far and 13 more are in the construction phase. Its Italian restaurant chain Toscano is also expected to open new stores and reach 20-25 stores in the next 2 years. It remains to be seen what obstacles will the company face in expanding the new restaurant chain and whether it will be able to scale up its delivery business in competition to 3rd party delivery majors like Dominos, Swiggy and Zomato. Nonetheless, given the good brand recall, wide geographical reach and the vast potential of the Indian Food Services sector, Barbeque Nation is an interesting stock to watch out for.

Disclaimer

This is not a piece of investment advice. Please read our terms and conditions.