About the Company

Blue Star is India’s leading air conditioning and commercial refrigeration company, with annual revenue of over ₹5200 crores (over US$ 750 million), a network of 32 offices, 5 modern manufacturing facilities, 2800 employees, and 2900 channel partners. The Company has 5000 stores for room ACs, packaged air conditioners, chillers, cold rooms as well as refrigeration products and systems, along with 765 service associates reaching out to customers in over 800 towns.

The Company fulfills the cooling requirements of a large number of corporate, commercial as well as residential customers. Blue Star has also forayed into the residential water purifiers business with a stylish and differentiated range including India’s first RO+UV Hot & Cold water purifier; as well as the air purifiers and air coolers businesses.

Blue Star’s other businesses include the marketing and maintenance of imported professional electronics and industrial products and systems, which is handled by a wholly-owned subsidiary of the Company called Blue Star Engineering & Electronics Ltd.

Q4 FY23 Updates

Financial Results & Highlights

Detailed Results:

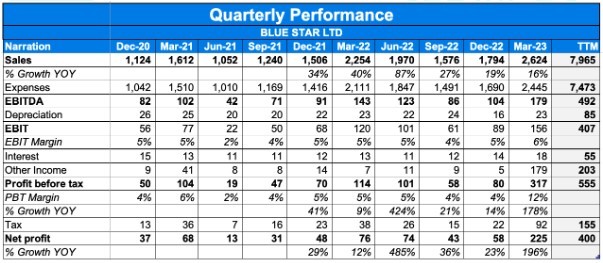

- The company had a consolidated revenue rise in Q4 of 16% YoY Rs. 2624 Cr vs Rs. 2254 Cr the previous year.

- EBIDTA for Q4 grew from Rs. 143 Cr at 6.3% margin in Q4FY22 to Rs. 179 Cr with 6.8% EBITDA margin in Q4FY23.

- FY23 consolidated revenue for the company grew by 32% to Rs. 7977 Cr from Rs. 6064 Cr the previous year.

- FY23 consolidated EBITDA stood at Rs. 493 Cr with 6.2% margin as compared to Rs. 346 Cr with 5.7% margin in FY22.

- Q4FY23 PBT was at Rs. 146 Cr with 5.6% margin vs the previous year at Rs. 114 Cr with 5.1% margin.

- FY23 PBT was at Rs. 385 Cr with 4.8% margin vs the previous year at Rs. 251 Cr with 4.1% margin.

- The company switched to Straight-Line method of Depreciation effective from Oct 1, 2022.

- The Capital Employed for the company as on Mar’23 was Rs. 1538 Cr vs Rs. 1088 Cr the previous year.

- The working capital was employed due to Investments in Capacity expansion projects at existing plants and the new plant at Sri City.

- Segment 1:- Electro-Mechanical Projects and Commercial Air Conditioning Systems :

- Q4FY23 Revenue grew by 10% at Rs. 1253 Cr vs Rs. 1140 Cr in Q4FY22

- Q4FY23 Result was at Rs. 99 Cr (7.9% margin) vs Rs. 76 Cr in Q4FY22 (6.7% margin)

- FY23 Revenue grew by 25% to Rs. 4016 Cr vs Rs. 3204 Cr in FY22

- FY23 Result was at Rs. 277 Cr (6.9% margin) vs Rs. 195 Cr in FY22 (6.1% margin)

- Expanded product portfolio and channel expansion enabled growth in revenue; demand from tier 3, 4 and 5 cities continued to be encouraging

- Business and economic activities in the Middle East markets continued to remain upbeat

- Carried forward order book for the segment was at Rs 4785 cr as of Mar 23 vs Rs 3034 cr as of Mar 22, a growth of 58%

- Segment 2:- Unitary Products :

- Q4FY23 Revenue grew by 22% at Rs. 1268 Cr vs Rs. 1037 Cr in Q4FY22

- Q4FY23 Result was at Rs. 107 Cr (8.4% margin) vs Rs. 72 Cr in Q4FY22 (7.0% margin)

- FY23 Revenue grew by 39% to Rs. 3627 Cr vs Rs. 2612 Cr in FY22

- FY23 Result was at Rs. 282 Cr (7.8% margin) vs Rs. 156 Cr in FY22 (6.0% margin)

- With the early onset of summers, witnessed a surge in demand for our room air conditioners and grew by 20% as compared to Q4FY22

- Grew faster than the market and ended the year with RAC market share of 13.5%

- Segment 3:- Professional Electronics and Industrial Systems :

- Q4FY23 Revenue grew by 33% at Rs. 103 Cr vs Rs. 78 Cr in Q4FY22

- Q4FY23 Result was at Rs. 20 Cr (19.2% margin) vs Rs. 14 Cr in Q4FY22 (18.5% margin)

- FY23 Revenue grew by 35% to Rs. 335 Cr vs Rs. 247 Cr in FY22

- FY23 Result was at Rs. 51 Cr (15.1% margin) vs Rs. 42 Cr in FY22 (17.2% margin)

- Major orders bagged from JSW Steel Limited, Tirumala Hospitals, Maruti Suzuki, Bharat Heavy Electricals Limited, HDFC Bank, to name a few

- Dividend of Rs. 12 per share recommended by the Board.

Investor Conference Call Highlights:

- The company is currently in its 80th year of operation and on Sep 27, it will complete its 80th year.

- The management admits that there is a hit in operations due to unseasonal rains, which were predicted by IMD before.

- The management gives a guidance of 20% for the full year market growth, despite the unseasonal rains and the festive season.

- The management explains that the climatic peak of summer has shifted gradually, what used to be in May last week, it moved to May middle, then it started peaking in April last week. And this year it peaked around March last week, as per the management’s guidance in an interview.

- The management states that the IMD prediction about temperature shooting up in Delhi areas may help the Jan to June market grow by up to 25%, with atleast 20% growth expected.

- The management clarifies that there is no excess inventory stocking or piling up, due to the West, East and South doing extremely well while the North battles with rains.

- The board has declared a dividend of Rs. 12 per share and has also declared a bonus of 1:1. Post bonus, the dividend will stand restated at Rs. 6 per share.

- During the quarter, the company sold a land parcel which has given a profit of 170 crores, net of tax around 139 crores.

- The management states that 2022 is a milestone for manufacturing, by setting up the modern room air conditioner plant in Sri City, Andhra Pradesh and the ultra-automated deep-freezer plant in Wada.

- The company’s strategy will also work on targeting the middle class in Tier 3,4,5,6 areas for the light commercial segment.

- In refrigeration, in addition to the affordable products, the management is looking at two main strategies in the deep freezer business and adjacent products.

- The management states that the company’s strategy for the MEP business to build the order book by first looking at the profitability factor of each order.

- The management states that it is purposely and strategically diversifying its order book away from commercial buildings like IT, hotels, hospitals.

- The management states the company’s vision of becoming a globally significant air conditioning and refrigeration player in the future.

- The Middle East business that the company entered in 2017, has grown into a $100 million business. The company is also setting more subsidiaries in the US and Europe.

- The Blue Star Engineering and Electronics subsidiary is at Rs. 330 Cr revenue today, which is expected to grow to 1000 crores in the near future, which will immensely contribute to the bottom line.

- The management has plans for the company to move into backward integration going forward.

- The management states a market share goal for the company at 15% by FY25, which currently stands at 13.5%.

- The company saw 40% of its sales coming through consumer finance schemes in FY23.

- The 100 crore grant received by the company from MR. Advani has been allowed to be utlised for only additional R&D work.

- The management states that the company shall have an annual capex of 250 to 300 crore for the next two years to build capacities in a modular manner.

- The management’s goal for next is 1 million units for which 6 lakh units will come from the Himachal Pradesh plant, 3 lakh from Sri City and 1 lakh outsourced products which will predominantly be window air conditioners.

- The company’s business in the middle east worth $100 million is entirely product exports from India which will continue going forward.

- The management states that the benefit Sri City has that it can receive imports from the nearby ports easily, which will help it to cater to the southern region which will contribute to 45% of All India Sales.

- The commercials building portfolio is currently one-third of the MEP business which used to be 80% a few years back. The company continues to focus on diversification.

- The management has a positive view on ONDC and sees e-commerce sales going to 20% in FY24 and upto 25% in two to three years.

Analyst’s View:

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen an excellent quarter which saw good revenues growth of 16% YoY. The company remains confident of the prospects of its EMP and MEP business given the policy support for the rise of the infra sector. It remains to be seen how the pricing environment and competition will fare in the industry going forward and how will the new opportunities in the EMP and commercial AC spaces evolve. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q3 FY23 Updates

Financial Results & Highlights

Detailed Results:

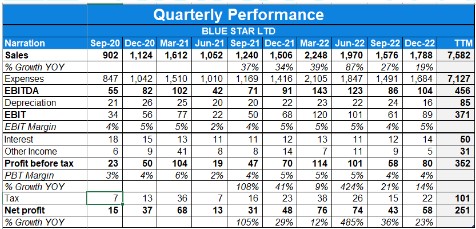

- The company had a consolidated revenue rise of 19% YoY.

- PBT was up to Rs 80 Cr vs Rs 70 Cr last year.

- EBIDTA grew from Rs.91 Cr to Rs.105 Cr YoY

- Order book for the company was up 92% YoY to Rs 4245 Cr. for 9MFy23.

- Carried-forward order book as of December 31, 2022, grew by 47.3% to a record Rs 4861.99 crore, compared to Rs 3301.33 crore as on December 31, 2021.

- Capital Employed as on December 31, 2022, increased to Rs 1505.56 crore as compared to Rs 1107.41 crore as on December 31, 2021, owing to higher inventory holding to prepare Blue Star Limited January 31, 2023 for the upcoming season and mitigate supply chain risks and capital investments for manufacturing capacity expansion projects, at Wada and by the subsidiary Blue Star Climatech Limited at its plant at Sri City

- Carried forward order book stood at Rs.4633 Crs for EMP & commercial Air-conditioning systems.

- Capital employed increased from 569 Cr to 648 Cr.

- Net borrowings were increased to Rs.396 Cr.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was up 34% YoY in Q3.

- Unitary products biz grew by 50% while professional electronics & industrial systems grew by 36%.

- The company ended the quarter with a net borrowing of Rs 395.85 crore (debt-equity ratio of 0.36 on a net basis) as compared to a net borrowing of Rs 165.11 crore (debt-equity ratio of 0.18 on a net basis) as on December 31, 2021.

Investor Conference Call Highlights:

- The management states that the risk management framework is comprehensive to handle challenges like capacity additions, competition in the room air conditioner business, the impact of inflationary pressure on project execution, etc.

- The depreciation method has been changed from the ‘written down value’ method to the ‘straight line method’ with effect from October 1, 2022. This led to a lower quarterly depreciation charge of Rs 10.80 crore.

- Major orders were received during the quarter from Bangalore Metro Rail Corporation Limited and Central Organisation for Railway Electrification in Electro-Mechanical Projects business.

- Major orders received in Commercial Air-Conditioning Systems during the quarter were from Udaipur Cement Works Ltd., Reliance Projects & Property, etc.

- In the export market, The pace of execution of projects and order inflow in Qatar witnessed a slowdown due to preparations and restrictions in the run-up to the FIFA World Cup while The operations of the joint venture in Malaysia continued to be impacted owing to a slowdown in construction and order finalizations amidst weak macroeconomic conditions in the country.

- In the Cooling and Purification Products business, The new plant at Sri City commenced commercial production in January 2023 and is expected to aid improvement in margins going forward.

- In the commercial refrigeration biz, major orders received during the quarter were from Reliance Retail, Dr. Reddy’s Pharma, Milma, Hatsun Agro, and several proprietary agro customers.

- In the Professional Electronics and Industrial Systems, revenues grew by 29% where Major orders were bagged from Arcelor Mittal Nippon Steel India Ltd., Indian Overseas Bank, Bharat Heavy Electricals Limited, ICICI Bank, and Hero MotoCorp to name a few.

- The management highlighting the benefits of Sri City stated that “there is a leverage in terms of logistics and working capital, as compared to the 10 to 12 days of transit inventory, any of the locations in the south can be served overnight from Sri City”.

- In Electro-Mechanical projects, the company continues to maintain the margin outlook at 6% to 6.5%

- In the cooling products segment, the company is targeting a share of 15% & EBITDA margins outlook for the segment remains unaltered at 8% to 8.5%

- Some major trends in the industry include less than 7% AC penetration Vs the expected 25% level & PLI scheme promoting indigenization and capacity expansion.

- The management explains that the company is the No. 1 player in the institutional segment and high-end residential customers and quite a few products that are required for that segment are premium, therefore under its Sri city facility, it will focus on bringing a different mix of products including affordable range.

- The company’s guidance of OPM of 8-8.5% factors in PLI, scale benefit, and operating leverage.

- Since the company’s Himachal facility is running at full utilization, therefore the Sri city facility will help in catering demand coupled with cost optimization. The facility is expected to break even in 3 years.

- The management highlighted tremendous growth opportunities in the industry by stating that “ If we consider room air-conditioners, a market size of Rs 17,500 crores looks very minuscule. The value of MEP projects getting finalized in a year is around Rs 6,500 crores which in our view is only 20% of what is required and the other 80% is an opportunity. That could drive consistent growth.”

- The company changed the depreciation policy since the expected life of its machine is 20 years, while using the WDV method leads to 70-75% depreciation being charged in the first year itself, therefore SLM will give a better representation of the value of assets & depreciation.

- The company capitalized capacities at Sri City and Wada plants in the current year and the total capitalization is in the region of around Rs.280 crores.

- The company does not have any plans to get into white goods & its strategy to deliver more shareholder value would be by widening product categories in which it is not present, indigenizing to improve margins, and expanding an international footprint that would create long-term value.

- In the PLI scheme, PLI benefit is only for sheet metals and powder coating and the company has not invested in motors, drives, and plastic injection molding. It will look to source these components from entities that have the PLI benefit in those categories.

- The company gained market share through an increased presence in certain underrepresented markets and widening the product portfolio.

- The management states that around 15% of annual sales will be coming in this financial year from Sri City.

- The company outsources only Window air-conditioners, which account for around 5% to 6% of its total sales.

Analyst’s View:

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen an excellent quarter which saw good revenues growth of 19% YoY. The company remains confident of the prospects of its EMP business given the policy support for the rise of the infra sector. It remains to be seen how the pricing environment and competition will fare in the industry going forward and how will the new opportunities in the EMP and commercial AC spaces evolve. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q2 FY23 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 1,411 | 1,094 | 28.98% | 1,848 | -23.65% | 5,377 | 3,842 | 39.95% |

| PBT | 41 | 33 | 24.24% | 91 | -54.95% | 196 | 98 | 100% |

| PAT | 30 | 21 | 42.86% | 67 | -55.22% | 128 | 66 | 93.94% |

| Consolidated Financials (in Crs) | ||||||||

| Q2FY23 | Q2FY22 | YoY % | Q1FY23 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 1,576 | 1,240 | 27.10% | 1,970 | -20% | 6,046 | 4,264 | 41.79% |

| PBT | 58 | 47 | 23.40% | 101 | -42.57% | 251 | 148 | 69.59% |

| PAT | 43 | 31 | 38.71% | 74 | -41.89% | 168 | 101 | 66.34% |

Detailed Results

- Company’s revenue grew +27.10 YoY vs down -20% QoQ on consolidated basis.

- Company’s PAT grew +38.71% YoY vs down – 41.89% QoQ on consolidated basis.

- Company reported EBIDTA growth of 21% YoY.

- Earnings per share grew 35% YoY.

- Carried Forward Order Book as on September 30, 2022, grew by 30.06% to Rs 4,162.05Cr compared to Rs 3,185.91Cr as on September 30, 2021.

- Net Borrowing as on September 30, 2022, was Rs 392.62 crores (debt equity ratio of 0.37) compared to Rs 44.34 crores as on September 30, 2021 (debt equity ratio of 0.05) owing to higher inventory holding to mitigate continuing supply chain disruptions and capital investments for the manufacturing capacity expansion projects.

- Consolidated Segment revenue growth for Q2FY23:

- EMP & Commercial Air Conditioning Systems:- 32.6% YoY

- Unitary Products:- 15.4% YoY

- Professional Electronics and Industrial Systems Business:- 49.9%

- H1FY23 Segment Financial Performance:

- EMP and Commercial Air-Conditioning systems

- Revenue Growth:- H1FY23 = Rs 1,753Cr vs H1FY22 Rs 1,229Cr Up +43%

- Capital Employed:- H11FY23 = Rs 413Cr vs H1FY22 Rs 337Cr

- ROCE:- H1FY23 = 62% vs H1FY22 = 33%

- Professional Electronics & Industrial Systems

- Revenue Growth:- H1FY23 = Rs 145Cr vs H1FY22 Rs 103Cr

- Unitary Products

- Revenue Growth:- H1FY23 = Rs 1,649Cr vs H1FY22 Rs 960Cr Up +72%

- Capital Employed:- H11FY23 = Rs 721Cr vs H1FY22 Rs 486Cr

- ROCE:- H1FY23 = 39% vs H1FY22 = 35%

- Net Borrowing:- H1FY23 = Rs 393Cr vs H1FY22 = Rs 44Cr

- Outlook

Company’s VC&MD said “The demand for our products and solutions from the segments in which we are operating, continues to be good now. With the push in infrastructure investments and the commencement of the capacity expansion cycle in the manufacturing segment, we expect order inflows in the Projects segment to remain buoyant throughout the year. Besides, the low level of penetration of room ACs in India is expected to aid market growth in the Room Air Conditioner business going forward. Opportunity for our Commercial Refrigeration business is also expected to be robust with the growing investments in food processing and the organized retail sectors. We are hopeful that the softening of commodity prices and a few localization initiatives will enable us to partly mitigate the impact of depreciation of the Indian Rupee against the US Dollar. Against the backdrop of the above factors, I remain optimistic about the prospects for our businesses in H2.”

Investor Conference Call Highlights

1.The company stated that B2B is still doing well, with record levels of order inflows and order finalizations. including a range of industries, including QSR, Metro Railway, Water Projects, and showroom.

- Even tho commodity prices are softening, company said. Because we have purchased the raw materials at old rates, the advantage of the commodity price softening will occur in H2FY23

- On H2FY23, the company is optimistic. due to India’s low rate of RAC penetration. a rise in the consumption of residential real estate.

- EBITDA Margins were 5.4% in Q2FY23 compared to 5.7% in Q2FY22. Due to increasing input prices in some divisions and greater spending, the operating margin declined in the second quarter of FY23.

- The company aims to achieve a 14% market share soon.

- Regarding the broader economy, the company stated that despite geopolitical uncertainties and the effects of the strengthening dollar, the Indian economy is still doing well. Both the public and private sectors’ CAPEX is positive.

- Comparing the Sri City factory to the Himachal facility will provide the company with a competitive advantage.

- The company expects commercial refrigeration industry growth of 20% CAGR.

- According to the company, the competitiveness is still quite strong. like always in the industry

- The company keeps holding large amounts of inventory to support the summer season’s revenue growth.

- The company stated that its market share varied across the nation. As a result, it is spending money on distribution expansion and product repositioning to increase its market share in areas where it is currently underrepresented.

- Segment wise update

- Electromechanical Projects

The company said that overall pace execution is good. The company noticed a significant increase in inquiries and order finalizations in the factories, metro railway, and data centre segments. Tenders continue to pour into the infrastructure sector. For an integrated data centre project, the company secured its largest-ever order in Q2FY23.

- Commercial Air Conditioning systems

Demand increased across all market segments, which increased CACS revenue. Company subsequently strengthened its positions in Tier 2, 3, and 4 towns, where these cities generated over 65% of the revenue.

Company continues to hold the top spot in conventional and inverter ducted air conditioning systems, scroll chillers, and VRFs, while placing second in screw chillers and VRFs.

- International Business

The company saw growth in every business segment. In order to serve new customer categories, the company significantly extended its offerings across markets. The company observed a significant demand for commercial refrigeration and air conditioning goods.

The company has established a fully owned subsidiary in the US. and received some orders from Tim Horton’s, Americana, and Domino’s.

- Cooling and purification products

Despite the typically low demand quarter, room air conditioning business grew by 17%.

Company grew in line with the market and maintained it’s Market share of 13.25%.

The Sri City project is progressing well and is expected to be open for production in Jan 2023.

- Commercial Refrigeration business

The demand for commercial refrigeration products increased across all market segments as consumption levels returned to normal. The retail sector’s demand for the items used in supermarket refrigeration remained positive. In this quarter, the demand for the hotel industry also increased.

The company kept up its position as a leader in deep freezers, storage water, and modular cold rooms.

- Professional Electronics and industrial systems.

The company observed a significant increase in the demand for medical diagnostic tools as a result of post-COVID investments and growing public awareness. Data security solutions for the BFSI sector, as well as non-destructive testing services, continued to be in high demand.

Company got major orders from Arcelor Mittal, Jindal saw, Hdfc bank, Tata steel and ICICI Bank.

- Company has started commercial production in its second plant in Wada in H1FY23.

- .Company increased its net borrowings to Rs390Cr in Q2FY23 vs Rs40Cr in Q2FY22. The company has used this cash to hold higher inventories and capacity expansion plans.

Analyst’s View

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has also done well to establish itself as one of the leading commercial cooling and electromechanical project solutions providers in India. Furthermore, the company has also expanded into the still underpenetrated water purifier segment where the vast majority of the addressable market remains untapped. The current quarter results were decent considering that it is an off-season for a cooling solutions provider like Blue Star. Although the margins for the quarter were low due to higher advertising expenses from signing Virat Kohli as the brand ambassador, the management seems to think that this is a temporary blip and margins should normalize going forward. It remains to be seen how long the current slowdown in the real estate and infra sectors will continue as this has restricted growth in the commercial cooling solutions business. The heightened ad expenses from investing in Virat Kohli a brand ambassador are also yet to be justified as it will take some time for these ad efforts to solidify the brand image. Nonetheless, given its robust market positioning and the big potential for all forms of cooling solutions and products in a tropical country like India, Blue Star is a good cooling solution stock to watch out for.

Q1 FY23 Updates

Financial Results & Highlights

Detailed Results:

- The company had a consolidated revenue rise of 87% YoY.

- PAT was up to Rs 74 Cr vs Rs 13 Cr last year.

- EBIDTA grew from Rs.42.23 Cr to Rs.123.31 Cr YoY, its margins increased to 6.3% from 4%.

- Carry forward order book for the company stood at Rs 3901 Cr.

- Capital employed increased from Rs.969 Cr to Rs.1018 Cr on account of capital investments for the capacity expansion projects at Wada and Sri City.

- Net borrowings in the previous year turned into a net cash balance this year at Rs.81 Cr in Q1.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was up 57% YoY in Q1. Orders Booked in Q1 was at Rs 1366 Cr vs Rs 651 Cr last year.

- The Carried-forward order book of the Electro-Mechanical Projects business was Rs 3655 Cr Vs Rs.3017 Cr.

- Blue Star was able to maintain its position as number 1 position in Ducted Air Conditioning, number 2 in VRF and moved up to number 2 in Chiller product categories.

- In the Unitary Products segment, the company saw revenue growth of 122% YoY in Q1.

- Unitary Products saw segment revenue of 1124 crore vs 505 crores the previous year for Q1. Segment Results were at 91 crore vs 22 crore the previous year.

- Professional Electronics and Industrial Systems reported a segment revenue of 53 crore vs 41 crore the previous year. Segment results were at 6 crore vs 6 crore the previous year.

- The company grew its market share to 13.3%.

- The commercial refrigeration business saw improvement in demand across all customer segments.

- Neeraj Basur, Group CFO has to left Blue Star in the previous quarter.

Investor Conference Call Highlights:

- Nikhil Sohoni has joined the company as its new Chief Financial Officer with effect from July 1, 2022 with over three decades of experience.

- The management remains optimistic for FY23, though there are several headwinds facing the company, it believes the silver linings will help the company to move forward.

- In the event of a slowdown, it takes time to impact the AC refrigeration industry and similarly the industry is the last to be impacted during a revival.

- This is because, air conditioning comes in post the construction of the building and homes, and is one of the last few items to be equipped by the owners.

- The company has redeemed June 2020 NCDs to the tune of 175 crore in June 2022.

- In EMP business, order inflows from commercial buildings, factories, data center and infrastructure picked up during the quarter.

- The company received major order from Bangalore Metro Rail Corporation worth 390 crore.

- The company has gained market share in all categories and continued to maintain No 1 market position in Conventional and Inverter Ducted Air Conditioning Systems and well as Scroll Chillers and second position in VRFs and Screw Chillers.

- Some of the major orders received during the quarter were from Reliance Industries, L&T – Railway Freight Corridor and Laxmi Diamonds.

- The newly entered markets of Nigeria, Bangladesh and Nepal have responded well to the launch of the new and improved applied range of products.

- The company has commenced the export of Deep Freezers to the Middle East.

- Order Inflow in international business grew by 9% while revenue grew by 38% as compared to the previous year.

- The company continued to maintain its leadership position in Deep Freezers, Storage water coolers and Modular cold rooms. It also launched a new range of visi-coolers with a wide capacity range.

- The company received large orders in the commercial refrigeration business from Reliance Retail and Macleod Pharma and from several individual mushroom proprietors.

- The newly constructed manufacturing facility at Wada commenced production during the quarter.

- For unitary products, the company increased its prices in the month of April and will review its prices again in the end of August.

- The BEE rating change did not result in any price increase, because the company had already launched future ready models in the quarters before.

- The management gives a guidance of 6% EBITDA margins for the short term with a healthy cash flow.

Analyst’s View:

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen an excellent quarter which saw good revenues growth. It saw a good resurgence in EMP business with segment revenues showing great growth. The demand for commercial refrigeration remains resilient and this demand is expected to continue from QSRs. The company remains confident of the prospects of its EMP business given the policy support for the rise of the infra sector. It also expects to preserve its market share of 15% in the RAC space and match the industry CAGR of 15-18%. The company is also commissioning additional capacity for the expected demand rise across RAC and commercial refrigeration segments. It remains to be seen how the pricing environment and competition will fare in the industry going forward and how will the new opportunities in the EMP and commercial AC spaces evolve. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q4 FY22 Updates

Financial Results & Highlights

| Consolidated Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 2253 | 1651 | 36.4% | 1519 | 48.3% | 6081 | 4325 | 40.6% |

| PBT | 113 | 104 | 8.6% | 70 | 58.9% | 250 | 147 | 70% |

| PAT | 76 | 68 | 11.7% | 47 | 61.7% | 168 | 100 | 68% |

| Standalone Financials (In Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 2005 | 1531 | 30.9% | 1339 | 49.7% | 5413 | 3904 | 38.6% |

| PBT | 91 | 97 | -6.1% | 57 | 59.6% | 195 | 98 | 98.9% |

| PAT | 59 | 65 | -9.2% | 38 | 55.2% | 127 | 65 | 95.3% |

Detailed Results:

- The company had a consolidated revenue rise of 36% YoY & 48% QoQ.

- PAT was up to Rs 76 Cr vs Rs 68 Cr last year.

- EBIDTA grew from Rs.102 Cr to Rs.143 Cr YoY, its margins increased to 6.4% from 6.3%.

- Carry forward order book for the company stood at Rs 3253 Cr.

- Capital employed increased from Rs.653 Cr to Rs.989 Cr on account of decreased working capital management.

- Net borrowings were increased to Rs.67 Cr in FY22.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was up 44% YoY in Q4. Orders Booked in FY22 was at Rs 3145 Cr vs Rs 2245 Cr last year.

- The Carried-forward order book of the Electro-Mechanical Projects business was Rs 3034 Cr Vs Rs.2839 Cr.

- Blue Star was able to maintain its position as number 1 position in Ducted Air Conditioning, number 2 in VRF and moved up to number 2 in Chiller product categories.

- In the unitary products segment, the company saw revenue growth of 32% YoY in Q4.

- The company grew its market share to 13.3%.

- The commercial refrigeration business saw improvement in demand across all customer segments.

- The board has approved a dividend of Rs 10 per share for FY22.

- Mr. Neeraj Basur, Group CFO has decided to leave Blue Star.

Investor Conference Call Highlights:

- The company implemented a price increase of 2% to 3% on April 1 to combat commodity price increases.

- The management has a very positive outlook for Q1 despite interest rate hikes.

- Offices followed by Metro rail were the largest contributors to the carry forwards order book of the EMP business.

- The management’s view on the growth of their international business in Middle East is very positive.

- Unitary products business faced headwinds in input costs and disruptions in supply chains which led to drop in segment margins.

- The company received breakthrough orders from top companies like Ola, Reliance, Dunzo, Zomato and Dmart for its commercial refrigeration products.

- Major order by the company for its segment 3 business were bagged from Axis Bank, Hdfc bank, Icici bank and Hal.

- The company’s new range of room ACs and commercial refrigeration is expected to significantly aid the growth in the upcoming quarters.

- Due to the ongoing conflict between Russia and Ukraine, the management expects input cost pressures and supply chain challenges to persist in the short term.

- The management states that 90% of the company’s buyers are first time buyers, 65% buyers are from tier – 3,4,5 markets and 45% of the sales are finance through consumer finance.

- To cater well to these first-time buyers, the company has introduced a new range of affordable premium air conditioners which are reengineered to have a cost reduction.

- The company has 22 models future ready considering the energy label change coming into effect on 1st July.

- Due to the PLI scheme, a component ecosystem is developing in India which is helping reduce the company’s dependence on China.

- The company plans to commence production at the Sri City facility in Q3 which will reduce logistics cost.

- The southern region of the country contributes to 45% of the company’s sales.

- The company continues to pursue its goal of 15% market share by 2025.

- The management expects the input costs to soften by the end of the year due to the inflation control measures being taken.

- The management expects the company to get back to 8% to 8.5% operating margin this year. A contributor to this will be reducing advertising expenses which is being followed by all industry peers.

- The management states that the company has adequate inventory to cater to 30% growth during the peak summer season.

- The company is no longer dependent on import of drives. Currently it still needs to import chips and compressors.

- The management expects penetration levels to reach 10% for the market from the current 6%.

- 17% of the company’s sales are taking place through the ecommerce channel.

- The management has stated that “For such a huge country like India, a market size of Rs 15,000 crores is very surprising, but good days are here, for next five years, it will be a golden period for room air conditioners, it will grow exponentially because of these factors.”

Analyst’s View:

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen an excellent quarter which saw good revenues growth of 36% YoY. It saw a good resurgence in EMP business with segment revenues showing great growth. The demand for commercial refrigeration remains resilient and this demand is expected to continue from QSRs. The company remains confident of the prospects of its EMP business given the policy support for the rise of the infra sector. It also expects to preserve its market share of 15% in the RAC space and match the industry CAGR of 15-18%. The company is also commissioning additional capacity for the expected demand rise across RAC and commercial refrigeration segments. It remains to be seen how the pricing environment and competition will fare in the industry going forward and how will the new opportunities in the EMP and commercial AC spaces evolve. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q3 FY22 Updates

Financial Results & Highlights

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 1519 | 1131 | 34.3% | 1247 | 21.8% | 3827 | 2674 | 43.1% |

| PBT | 70 | 49 | 42.8% | 47 | 48.9% | 137 | 43 | 218.6% |

| PAT | 47 | 36 | 30.5% | 31 | 51.6% | 91 | 32 | 184.3% |

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 1340 | 1027 | 30.4% | 1103 | 21.4% | 3407 | 2373 | 43.5% |

| PBT | 57 | 33 | 72.7% | 32 | 78.1% | 104 | 1 | 10,300% |

| PAT | 38 | 23 | 152.1% | 21 | 80.9% | 68 | 1 | 6,700% |

Detailed Results:

- The company had a consolidated revenue rise of 34% YoY & 22% QoQ.

- PAT was up to Rs 47 Cr vs Rs 36 Cr last year.

- EBIDTA grew from Rs.82 Cr to Rs.91 Cr YoY, however its margins decreased from 7.2% to 6% due to continued input cost pressure.

- Carry forward order book for the company was up 2% YoY to Rs 3111 Cr.

- Capital employed increased from Rs.742 Cr to Rs.978 Cr on account of improved working capital management.

- Net borrowings were increased to Rs.165 Cr in YTD.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was up 42% YoY in Q3. Order inflow in Q3 was at Rs 830 Cr vs Rs 585 Cr last year.

- The Carried-forward order book of the Electro-Mechanical Projects business was Rs 2311 Cr Vs Rs.2217 Cr. Major orders gotten in Q3 were from were from Avenue Supermarts, DSR Builders, Olympia Cyberspace and JSW Steel.

- Blue Star was able to maintain its position as number 1 position in Ducted Air Conditioning, number 2 in VRF and moved up to number 2 in Chiller product categories.

- In the unitary products segment, the company saw revenue growth of 45% YoY in Q3.

- Blue Star had applied for the PLI benefit for sheet metal components and heat exchangers. The application has now been approved as earlier envisaged.

- The company grew its market share to 13.25%.

- The commercial refrigeration business saw improvement in demand across all customer segments.

- Professional electronics and industrial systems grew revenue by 47% YoY in Q3.

Investor Conference Call Highlights:

- Revival of business and economic activity enabled the company to end the quarter on a strong note with all segments witnessing robust volume growth and surpassing pre-pandemic levels.

- The impact of an increase in commodity prices, raw materials, and ocean freight and rollback and cuts in discretionary spending that the company had undertaken in FY’21 have led to lower EBITDA in Q3.

- The company’s EMP business driven by the CAPEX commitments of the private sector received order inflows from Factories and Light Industrial sectors. The inflow of orders from Infrastructure, NEP, and water distribution picked up during the quarter.

- The growth of QSRs in Middle East markets led to improve in demand for refrigeration solutions. The company also witnessed good traction for its products in the newly entered market of Tanzania.

- The management continues to explore new markets internationally for business opportunities and expansion.

- The construction of the new factory at Sri City is progressing as planned and is expected to be commissioned by October ’22.

- The company continued to maintain its leadership position in deep freezers, storage water coolers, and modular cold rooms.

- In Professional Electronics & Industrial Systems, major orders were backed from JSW Steel, ICICI Bank, FIS Payment Solutions, and Reliance Industries.

- The management expects the disruption due to the third wave to continue till the end of Feb. They anticipate the peak selling months starting from march to be unaffected.

- The management continues to remain optimistic about the growth prospects in the project business across the select customer segments focused on them. Increased CAPEX investments by both the public and private sectors are expected to offer good prospects for the Electro-Mechanical Projects business.

- The management expects margins to remain impacted in the short term while revenue growth to be robust. Prudent working capital management is expected to result in healthy cash flows and a strong balance sheet.

- The room AC market grew by 25% and the company grew in the segment by 28% due to encouraging demand in December.

- The company had already taken 3 price hikes in 2021 so no price hikes were taken in Q3. The management does not plan any price hikes for Q4 either despite there being pressures on margins.

- The management expects the margin profile to be better from Q4 due to the competitive pressure easing and the third wave not impacting as severely as the earlier ones.

- The management sees the AC market growing at 15% – 18% CAGR in FY’23.

- The management plans to scale up the company’s market share to 15% in the coming years by growing faster than the market consistently.

- The company’s unallocable expenses are in the range of 1.5% to 1.7% of overall revenues which is in a healthy ballpark range as compared to peers according to the management.

- In the past calendar year, the company has taken a 15% price increase in three installments.

- The number of stores the company is serving has gone up 15%-20% YoY. Currently, it stands at 7,500 in Q3. The company plans to reach 8000 stores by end of 2022.

- The management expects to commission the second deep freezer manufacturing plant at Wada in the next three months.

- The plant under construction in Sri City is expected to get commissioned by October to December this year. This plant has received the PLI benefit as well.

- The current contribution to sales from e-commerce for the overall market was 10% and for the company was 8%.

Analyst’s View:

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen an excellent quarter which saw good revenues growth of 37% YoY. It saw a good resurgence in EMP business with segment revenues rising 42% YoY here. The demand for commercial refrigeration remains resilient and this demand is expected to continue from QSRs. The company remains confident of the prospects of its EMP business given the policy support for the rise of the infra sector. It also expects to preserve its market share of 15% in the RAC space and match the industry CAGR of 15-18%. The company is also commissioning additional capacity for the expected demand rise across RAC and commercial refrigeration segments. It remains to be seen how the pricing environment and competition will fare in the industry going forward and how will the new opportunities in the EMP and commercial AC spaces evolve. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q2 FY22 Updates

Financial Results & Highlights

| Consolidated Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 1248 | 908 | 37.44% | 1060 | 17.74% | 2308 | 1543 | 49.58% |

| PBT | 47 | 23 | 104.35% | 19 | 147.37% | 67 | -6 | -1216.7% |

| PAT | 31 | 15 | 106.67% | 13 | 138.46% | 44 | -4 | ######## |

| Standalone Financials (In Crs) | ||||||||

| Q2FY22 | Q2FY21 | YoY % | Q1FY22 | QoQ % | H1FY22 | H1FY21 | YoY% | |

| Sales | 1104 | 812 | 35.96% | 964 | 14.52% | 2068 | 1345 | 53.75% |

| PBT | 33 | 12 | 175% | 14 | 135.71% | 47 | -32 | -247% |

| PAT | 21 | 8 | 163% | 9 | 133.33% | 30 | -23 | -230.43% |

Detailed Results:

- The company had a consolidated revenue rise of 37.4% YoY & 17.7% QoQ.

- PAT was up to Rs 31 Cr vs Rs 15 Cr last year.

- EBIDTA grew from Rs.55 Cr to Rs.70.7 Cr YoY, however its margins decreased from 6.1% to 5.7%.

- Carry forward order book for the company was up 5.5% YoY to Rs 3185.9 Cr

- Capital employed decreased from Rs.1124 Cr to Rs.938.4 Cr on account of improved working capital management.

- Net borrowings were reduced to Rs.44 Cr in H1.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was up 33.8% YoY in Q2. Order inflow in Q2 was at Rs 709 Cr vs Rs 685 Cr last year.

- The Carried-forward order book of the Electro-Mechanical Projects business was Rs 2240 Cr Vs Rs.2070 Cr. Major orders gotten in Q2 were from were from L&W Construction, Embassy Realty and Max Square.

- Blue Star was able to maintain its position as number 1 position in Ducted Air Conditioning, number 2 in VRF and number 3 in Chiller product categories.

- Major orders bagged in Q2 for commercial AC systems were from Late Meenatai Thackeray COVID Hospital NMMC, Bharatiya Reserve Bank Note Mudra (Mysore), NTPC, Reliance Retail, ONGC, and ISRO (Sriharikota).

- In the unitary products segment, the company saw revenue growth of 42.7% YoY in Q2.

- Blue Star has applied for the PLI benefit for sheet metal components and heat exchangers.

- The company maintained its market share at 13%.

- The commercial refrigeration business saw improvement in demand across all customer segments.

- The company bagged major orders in commercial refrigeration from Reliance Retail, ITC Fortune Hotel, SRL Limited, Omega Systems and Zydus Cadila.

- Professional electronics and industrial systems grew revenue by 44.5% YoY in Q2. This segment’s contribution to total revenue decreased to 16% from 19% YoY due to change in product mix.

- Data Security Solutions business continued to do well.

- Major orders were bagged from State Bank of India, Federal Bank, HDFC Bank, Bharat Electronics, Jio platform to name a few.

Investor Conference Call Highlights:

- The company faced headwinds around raw materials and other input cost increases leading to price hikes in its products and thus the cost increase has been passed to the customers. This was the case for every player in the industry

- The higher inventory carried forward from Q1 was liquidated.

- The management is increasing its focus on the light industrial sector i.e infrastructure such as metro rail, electric substations, factories, data centers, warehousing, health care since these are the customer segments that are revising strongly.

- The management feels that the growth in infrastructure projects will be able to compensate for the soft demand in commercial real estate.

- The PLI scheme targeting manufacturing capex as well the growth in E-Commerce is leading to an increase in warehouse storage, which are favorable developments for the industry.

- The company has taken price hikes of 12-14% since January which have been partially offset by input cost inflation.

- The management is guiding towards reaching its normalized margin profile by Q4.

- The company has been able to increase the revenue share of the Northern region to 35% of total revenue through expansion of dealership channels & mass premium range of product offering. South India contributed 35% of total revenues followed by West & East.

- The management believes that demand for commercial refrigeration spiked for short period and now it has matured due to mass vaccination of the public. However, Blue Star expects good demand going forward from supermarkets & educational institutions.

- The management expects the Sri city expansion to get commissioned by Oct 2022. This greenfield project will have a capacity greater than the Himachal plant & it will be used to first cater to the domestic market & then export markets will be considered. Sales from this plant are expected to come in from FY24.

- The company incurred capital expenditure for expanding its deep freezer production capacity which is getting commissioned in the next couple of months in Wada, inventory impact & capital expenditure for Sri city expansion leading to capital employed in the unitary product segment.

- Regulatory requirements to address data confidentiality and security concerns, and substantial enhancement of digitization and the digital footprint across most business processes are the prime factors driving growth in the data center industry in India according to the management.

- The company expects good demand in Q3 due to the festival season.

- The effective tax rate would be in the range of 28% to 30% despite the move into the new tax regime of 22% + surcharge.

- The company will incur a normal CapEx of close to Rs.100 Crs in FY22.

Analyst’s View:

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen a good quarter which saw good growth YoY across all segments especially the unitary products despite cost pressure from raw material price rises. It saw a resilient performance in EMP and commercial AC segments while the UCP segment saw a rise due despite the extended monsoon. The demand for commercial refrigeration remains resilient and this demand is expected to continue from supermarket chains and educational institutions. The company is also looking to target infra sectors like metro stations, airports, data centers, and others to make up for the loss in demand for the EMP business from traditional sources like commercial real estate. It remains to be seen how the pricing environment and competition will fare in the industry going forward and how will the new opportunities in the EMP and commercial AC spaces evolve. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q1 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 964 | 534 | 80.52% | 1531 | -37.03% |

| PBT | 14 | -44 | 131.82% | 98 | -85.71% |

| PAT | 9 | -31 | 129.03% | 65 | -86.15% |

| Consolidated Financials (In Crs) | |||||

| Q1FY22 | Q1FY21 | YoY % | Q4FY21 | QoQ % | |

| Sales | 1060 | 635 | 66.93% | 1651 | -35.80% |

| PBT | 19 | -29 | 166% | 103 | -81.55% |

| PAT | 13 | -20 | 165% | 67 | -80.60% |

Detailed Results:

- The company had a consolidated revenue rise of 67% YoY in Q1 but it fell 36% QoQ.

- PAT was up to Rs 13 Cr vs a loss of Rs 20 Cr last year.

- Carry forward order book for the company was up 8% YoY at Rs 3152.3 Cr as of 30th June 2021.

- Net borrowings were reduced to 68.47 Cr in Q1.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was up 61.7% YoY in Q1. Order inflow in Q1 was at Rs 650.78 Cr vs Rs 266.78 Cr last year.

- The Carried-forward order book of the Electro-Mechanical Projects business was Rs 2232 Cr as of 30th June 2021. Major order gotten in Q1 were from Ola Electric in TN and Netmagic IT Services in Mumbai.

- The commercial AC business saw revenue growth of 108% YoY in Q1. Blue Star was able to maintain its position as number 1 position in Ducted Air Conditioning, number 2 in VRF and

number 3 in Chiller product categories. - Major orders bagged in Q1 were MRDA Covid Hospitals (Mumbai), SALCOMP (Chennai),

Reliance Zoo (Jamnagar), Kalinga Institute of Technology (Bhubaneswar) and Adichuchanagiri

Institute of Medical Sciences (Bangalore). - In the unitary products segment, the company saw revenue growth of 83.9% YoY in Q1.

- RAC market in India grew 55% YoY in Q1. The company maintained its market share at 13% and grew RAC business 58% YoY in Q1.

- The commercial refrigeration business saw improvement in demand across all customer segments.

- The company bagged major orders in commercial refrigeration from Biological E, Gland Pharma, Ascent Pharma and Zydus Cadila among others.

- The Professional Electronics and Industrial Systems business saw revenue rise to Rs 41.4 Cr from Rs 38.7 Cr last year.

- Major orders were bagged in Q1 from Man Industries, Central Imaging & Diagnostic, Canara Bank, ICICI Bank, MRF, etc.

Investor Conference Call Highlights:

- EBITDA margin in Q1 was at 4%.

- The major reason for the bad performance in Q1 was the detrimental impact on the peak season for RACs due to the 2nd wave of COVID-19.

- The EMP business saw slow execution in Q1 due to phased lockdowns.

- Delays in order finalization due to uncertainties impacted order inflows from the commercial building sector.

- The company expects good opportunities to come for the EMP business from infra projects involving metro railways, electrical substations, water distribution, factories, data centers, and warehousing.

- Demand from builders and developers, marriage halls, auditoriums, hotels, and restaurants for the commercial AC business is yet to come back.

- Around 60% of sales in unitary products were from RACs while the rest was from other products.

- The management expects to come back to the 8% margin level in this business by Q4FY22 if there isn’t any major damage from the 3rd wave.

- The management expects the margin from unitary products to remain close to 6% as in FY21 due to the bad peak season in Q1.

- The company had taken a price increase of 5% in Q4FY21 and 3% in Q1FY22.

- The margins have stayed down despite the price increases as some operating costs were back to normal, but revenues were subdued in Q1 which led to discounts and incentives which further put pressure on margins.

- E-commerce channel accounts for almost 15% of industry sales. For Blue Star, e-commerce accounts for 13-14% of UCP sales.

- The in-house manufacturing share for Blue Star was at 70% and it is expected to stay at this level going forward.

- The mass premium range has seen good traction and should perform well in the upcoming festive season.

- The PLI scheme is currently available only for components and not for finished products in the RAC industry. The company has yet to decide on how to go about this.

- The company’s sales in the North Zone have increased to 40% of overall sales and this was mainly on account of the extended summer season.

- The South Zone was subdued due to early rains and COVID restrictions, but it should normalize by the festive season according to the management.

- The management has yet to decide on whether to do another price rise to bring back margins to normal levels and it will decide in Q3 on how to proceed on this.

- Although the traditional customer segments of EMP like commercial real estate and private infra have yet to normalize, the company sees additional demand coming up from emerging segments like e-commerce warehouses, data centers, and others.

- The company will continue to operate in the EMP space with its credit profile-centric approach which has helped it maintain margins at 4-4.5% currently and is expected to bring it back to 5-5.5% as normalcy comes back.

- The gross debt remained at Rs 450 Cr.

- The management is optimistic of reaching a 14% market share in UCP by the end of the year.

- Around 58% of RACs sold in Q1 were inverter ACs.

- The company hopes to capture Rs 75-100 Cr of sales from the vaccine refrigeration opportunity in the year.

Analyst’s View:

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen a mixed quarter which saw good growth YoY but a decline in QoQ due to the 2nd wave of COVID-19. It saw a resilient performance in EMP and commercial AC segments while the UCP segment saw a decline due to falling sales in the peak season and high discounting. The company has already done a price increase of >8% since Jan but much of this has been dented due to discounting which is expected to continue till the festive season. The demand for end-to-end cold chain products remains resilient and has replaced traditional demand from restaurants and others for the commercial refrigeration business. It remains to be seen how the pricing environment and competition will fare in the industry going forward and how will the new opportunities in the EMP and commercial AC spaces evolve. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q4FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 1531 | 1231 | 24.37% | 1028 | 48.93% | 3904 | 4660 | -16.22% |

| PBT | 98 | 35 | 180.00% | 33 | 196.97% | 98 | 168 | -41.67% |

| PAT | 65 | 33 | 96.97% | 24 | 170.83% | 66 | 121 | -45.45% |

| Consolidated Financials (In Crs) | ||||||||

| Q4FY21 | Q4FY20 | YoY % | Q3FY21 | QoQ % | FY21 | FY20 | YoY% | |

| Sales | 1651 | 1306 | 26.42% | 1132 | 45.85% | 4326 | 5405 | -19.96% |

| PBT | 103 | 12 | 758% | 49 | 110.20% | 145 | 206 | -29.61% |

| PAT | 67 | 8 | 738% | 36 | 86.11% | 98 | 141 | -30.50% |

Detailed Results

- The company had a consolidated revenue rise of 26% YoY in Q4. PAT was up to Rs 67 Cr vs Rs 8 Cr last year, mainly due to the low base last year.

- FY21 performance for the company was dismal due to Q1 performance. Revenues in FY21 were down 20% YoY while PAT was at Rs 98 Cr vs Rs 141 Cr last year.

- Other income included Rs 32 Cr from the sale of property in Mumbai.

- Carry forward order book for the company was flat YoY at Rs 2952 Cr as of 31st Mar 2021.

- Net borrowings reduced by Rs 282.46 Cr in Q4. The company ended with a net positive cash balance of Rs 151.45 Cr as of 31st Mar 2021.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was up 18% YoY in Q4. Order inflow in FY21 was at Rs 2245 Cr vs Rs 3105 Cr in FY20.

- The Carried-forward order book of the Electro-Mechanical Projects business was Rs 2149 Cr as of 31st Mar 2021.

- The segment-wise breakup of the order book is:

- Office (IT/Non-IT): 29%

- Metro Rail: 22%

- Hospitals: 9%

- Industrial: 9%

- Power Generation & Distribution: 6%

- Malls: 4%

- Others (airports, hotels, educational institutions, etc.): 21%

- The commercial AC business saw revenue growth of 19% YoY in Q4. Major orders bagged in Q4FY21 were from Birla Cement (Nagpur), Avenue Supermart (Vijaywada/Surat), ISRO (Bangalore), Flextronics (Chennai), Gujarat Biotechnology (Ahmedabad), and West Coast Pharmaceuticals (Ahmedabad).

- Improved demand for cooling products in the Middle East markets enabled recovery for our International Business during the quarter. The upcoming EXPO 2020 in Dubai and the FIFA tournament in Qatar are expected to offer growth opportunities. The projects businesses in Qatar and Malaysia continued to be impacted owing to Covid.

- In the unitary products segment, the company saw revenue growth of 31% YoY in Q4. FY21 revenues were down 18.8% YoY.

- RAC market in India grew 27% YoY in Q4. The company increased its market share to 13.25% and grew RAC business 33% YoY.

- The commercial refrigeration business saw improvement n demand across all customer segments coupled with aggressive stocking by the channel. Blue Star launched a new range of pharma cold rooms, medical freezers, ice-lined refrigerators, and vaccine transporters, which were well received by the government, vaccine manufacturers, and private distributors.

- The company bagged major orders in commercial refrigeration from Dr. Reddy’s Labs, Apollo, Aurobindo Pharma, Zydus Cadila, Rebel Foods, Swiggy, Reliance Retail, etc.

- The Professional Electronics and Industrial Systems business saw revenue rise to Rs 50 Cr from Rs 43 Cr last year.

- Major orders were bagged in Q4FY21 from FIS Payment Solutions and Services, Navodaya Education Trust, Jio Platforms Limited, IndusInd Bank Limited, ICICI Bank Limited, etc.

- The Directors have recommended a dividend of Rs 4 per share.

Investor Conference Call Highlights

- Muted government expenditure also impacted order inflows in the infrastructure sector. Order inflows from the factories and light industrial sector improved as compared to last year, driven by the Make in India initiatives of the government.

- Factories, data centers, and warehousing sectors are also expected to show a good opportunity in the upcoming quarters.

- Stocking of inventory by channel ahead of the peak selling season, the improved share of billing from the e-commerce channel, and a general business sentiment improvement enabled growth in revenue for the room air conditioner business in Q4.

- Blue Star achieved a market share of 3% in water purifiers with a major share of billings to e-commerce players. It also reached breakeven in the product and has decided that water purifiers will be an e-commerce-centric product portfolio going forward.

- The material impact on sales from COVID-related restrictions in April appears to be 20% according to the management.

- Competitive intensity has risen from all the external price pressures from raw material, input costs, and increased freight costs.

- Order inflow for FY21 was Rs 2244 Cr vs Rs 3104 Cr last year.

- The company has had to increase prices by 3-5% to mitigate the recent rise in input costs.

- There have been cost rationalizations across the board but some of them will be back once normal business activity resumes.

- The usual demand from restaurants and others for commercial refrigeration has been muted but it has been replaced by demand from health care, pharma, food processing to the delivery segment.

- The management expects the traditional customers to recover once the COVID situation normalizes.

- Water coolers have seen slow offtake as this segment is mainly for government institutions, educational institutions, and others that are yet to recover fully.

- Blue Star is going to moderate the production pace for the next 2 or 3 months because it has sufficient stocks to sell in the background of the current disruption, according to the management.

- The company aims to neutralize the downward impact of some of the input cost increases and keep the margin near 8%.

- There isn’t much pressure on margin from MEP projects as they are fixed in nature and most cases contain procurement price protection. Thus only project overshooting project time would be causing margin pressure.

- Currently, the non-AC segment accounts for 40% of unitary products business. The largest share in the non-AC segment is from commercial refrigeration. Although the management is optimistic about the growth prospects of the RAC segment, the others should help in reducing the dependence on it and diversify revenue sources.

- Although the company is not looking to apply for the PLI license, it is expected to benefit indirectly from it.

Analyst’s View

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen a decent recovery in revenues and profits for Q4FY21. It saw a good recovery in all businesses including the RAC segment which outpaced industry growth and saw the company’s market share rise to 13.25%. The company has done well to rationalize inventory and order ahead for raw materials and institute price increases of 3-5% which has helped it counter the RM price inflation. The demand for end-to-end cold chain products remains resilient and has replaced traditional demand from restaurants and others for the commercial refrigeration business. It has also seen good growth in the water purifier segment achieving breakeven and reaching a market share of 3%. It remains to be seen what disruptions the company will have to face from the RM shortage and the impact on consumer behavior from the 2nd wave of COVID-19. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q3FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 1028 | 1068 | -3.75% | 812 | 26.60% | 2373 | 3628 | -34.59% |

| PBT | 33 | 5 | 560.00% | 12 | 175.00% | 1 | 132 | -99.24% |

| PAT | 24 | 1 | 2300.00% | 8 | 200.00% | 1 | 88 | -98.86% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY21 | Q3FY20 | YoY % | Q2FY21 | QoQ % | 9MFY21 | 9MFY20 | YoY% | |

| Sales | 1132 | 1242 | -8.86% | 908 | 24.67% | 2675 | 4099 | -34.74% |

| PBT | 49 | 32 | 53% | 22 | 122.73% | 42 | 194 | -78.35% |

| PAT | 37 | 20 | 85% | 15 | 146.67% | 32 | 134 | -76.12% |

Detailed Results

- The company had a consolidated revenue decline of 9% YoY in Q3. PAT was up 85% YoY at Rs 37 Cr.

- 9M performance for the company was dismal due to Q1 performance. Revenues in 9M were down 35% YoY while PAT was at Rs 32 Cr vs Rs 134 Cr last year.

- Carry forward order book for the company grew 12.3% YoY to Rs 3157 Cr as of 31st Dec 2020.

- Net borrowings reduced to Rs 131 Cr from Rs 344 Cr in Sep 2020. Debt to equity was at 0.16 times.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was down 32.9% YoY in Q3. Order inflow in Q3 was at Rs 637 Cr which was up 15.6% QoQ.

- The Carried-forward order book of the Electro-Mechanical Projects business was Rs 2217 Cr as of 31st Dec 2020.

- The commercial AC business saw a partial recovery in Q3. Major orders bagged in Q3FY21 were from Avenue Supermart (All India), Food & Drug Laboratory (Baroda), Prime Hospital (Roorke), ISRO Mahendragiri (Bangalore), and Larsen & Toubro Ltd (Bangalore).

- Improved demand for cooling products in the Middle East markets enabled recovery for our International Business during the quarter.

- In the unitary products segment, the company saw revenue growth of 17.3% YoY in Q3. Segment EBIT was up almost 5 times YoY at Rs 38.8 Cr.

- RAC market in India grew 25% YoY in Q3. The company maintained a market share of 13% and grew 32% YoY RAC business. It intends to participate in the RAC PLI scheme announced by the Govt of India. Blue Star also announced a price increase between 4% to 6% with effect from January 1, 2021.

- The commercial refrigeration business saw good recovery with traction coming from investments into the vaccination cold chain. Blue Star has been receiving orders from Government and private sector players investing in the augmentation of the cold chain for the vaccine inoculation program.

- The company bagged major orders in commercial refrigeration from SK Logistics, Metropolis, and Riveraa Labs, Keimed and CMC, Vellore.

- The Professional Electronics and Industrial Systems business saw revenue fall to Rs 45 Cr from Rs 57 Cr last year.

- Opportunities from the BFSI sector for the Data Security Solutions business, increased order inflow from the healthcare sector, a pick-up in orders from the industrial sector for material testing, and growth in orders from the essential services of the government sector drove revenue during the quarter.

Investor Conference Call Highlights

- Inquires in other markets such as SAARC, ASEAN and Africa improved during the quarter.

- The upcoming Expo 2021 in Dubai is expected to offer good opportunities in the construction sector for Blue Star.

- The company owns 20 acres of land in Sri City, apart from potential expansion opportunities at the Himachal Pradesh location.

- There has been pre-buying going on at the dealer level in anticipation of a string summer and the price rise of raw materials which is to be reflected in Q4.

- The employee cost reduction taken by Blue Star is likely to be rolled back in the future as the business recovers.

- In the PLI scheme announced for RACs, around Rs 3000 Cr is expected to be for finished goods and Rs 2000 Cr is expected to be for components.

- The management doesn’t think that the recent ban on CBU imports has contributed significantly to the market share rise for Blue Star. It has also stated that it has impacted mid and small-size players mostly.

- The PLI scheme for RACs is expected to be similar to the mobile PLI scheme. Both are expected to run for 5 years.

- The management sees the PLI scheme as a good opportunity to solidify its presence in the SAARC and ASEAN regions.

- Water purifier business is expected to become breakeven by the end of FY21.

- Margin profile is expected to remain stable in Q4 and there is also some room for overall growth in the coming quarter according to management.

- The company is making close to 100% of its IDUs in-house. It had also taken the buying decisions for Q4 in Q3 itself so it was not affected too badly by the container shortage.

- The container issues are expected to be normalized by March or April.

- the cold chain opportunity for vaccination drives is expected to be Rs 200 Cr or more for Blue Star. The vaccinations will be happening in phases and so the demand for this is not expected to be a flash in the pan and will be spread out over many quarters.

- The company may also operate under the PLI scheme for components and supply electronics for RACs but it will not be looking to get into the compressor space as it has different economies of scale and requires different levels of investment than Blue Star wants to do.

- E-commerce sales were at 6% in Q3.

Analyst’s View

Blue Star is one of the largest cooling solutions providers in the country. It is one of the biggest branded players in the RAC market. The company has seen a decent recovery in revenues and profits for Q3FY21. It saw a good recovery in the RAC business which also saw the company’s market share rise to 13%. The company has done well to rationalize inventory and order ahead for raw materials which helped it stave off the threat from the container shortage. There are a few big opportunities for Blue Star on the horizon like the RAC PLI scheme and the demand for the cold chain for vaccination drives. It has also seen good growth in the water purifier segment where it expects to achieve breakeven by the end of FY21. It remains to be seen whether the estimations of industry revival remain on track as mentioned by the management and whether disruptions from container shortage and the rise in raw material prices go away soon. Nonetheless, given the company’s strong market presence, its history of completing EMP projects, and its robust presence in semi-urban and rural India, Blue Star is a pivotal white goods stock to watch out for.

Q2FY21 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 812 | 1066 | -23.83% | 534 | 52.06% | 1345 | 2560 | -47.46% |

| PBT | 12 | 23 | -47.83% | -44 | 127.27% | -32 | 127 | -125.20% |

| PAT | 8 | 13 | -38.46% | -31 | 125.81% | -23 | 87 | -126.44% |

| Consolidated Financials (In Crs) | ||||||||

| Q2FY21 | Q2FY20 | YoY % | Q1FY21 | QoQ % | H1FY21 | H1FY20 | YoY | |

| Sales | 908 | 1260 | -27.94% | 635 | 42.99% | 1543 | 2857 | -45.99% |

| PBT | 22 | 54 | -59.26% | -29 | 175.86% | -7 | 162 | -104.32% |

| PAT | 15 | 37 | -59.46% | -20 | 175.00% | -4 | 115 | -103.48% |

Detailed Results

- The company had a consolidated revenue decline of 28% YoY in Q2. PAT was down 59% YoY at Rs 15 Cr.

- H1 performance for the company was dismal due to Q1 performance. Revenues in H1 were down 46% YoY while H1 PAT was at a loss of Rs 4 Cr.

- Carry forward order book for the company grew slightly to Rs 3019 Cr as of 30th Sep 2020.

- Net borrowings increased to Rs 344 Cr from Rs 189 Cr a year ago. Debt to equity was at 0.44 times. Net borrowings have reduced by Rs 84.47 Cr in Q2FY21.

- The company launched a new range of products embedded with ‘Virus Deactivation Technology’.

- Segment revenue for the Electro-Mechanical Projects & Packaged Air Conditioning Systems was down 31% YoY in Q2. Order inflow in Q2 was reduced to Rs 685 Cr which was down 13.8% YoY.

- The company won an Electrical & Mechanical works (E&M) order valued at Rs 149 Cr for ‘Mumbai Metro Line III, Package UGC-03’ for five underground stations from Mumbai Central to Worli, from Dogus-Soma JV.

- The Carried-forward order book of the Electro-Mechanical Projects business was Rs 2070 Cr as of 30th Sep 2020.

- Commercial AC business saw a partial recovery in Q2. Major orders bagged in Q2FY21 were from Greenfield Electronic Manufacturing Clusters (Hyderabad), Vijayanagar Institute of Medical Science (Bellary), Grand Hyatt Hotel (Bharuch), INTAS Pharmaceuticals (Ahmedabad), and National Mineral Development Corporation (Chandigarh).

- The demand for retrofit and revamp solutions with Virus Deactivation Technology is robust. Major orders for products and solutions such as duct cleaning, UVC emitters, filters, and fresh air augmentation have been received from ICICI Bank, Mercedes Benz India, and Airport Authority of India.

- In the unitary products segment, the company saw a revenue decline of 15.5% YoY in Q2. Segment EBIT was flat YoY. The company maintained a market share of 12.75% and is expecting this market to fully recover by December.

- Commercial refrigeration business saw good recovery with good traction from pharma and healthcare segments for its Modular Cold Rooms and Medical Refrigeration Products. Demand recovery is expected to accelerate with the opening of restaurants and other unlock measures and order inflows from local and national retail chains in the Supermarket Refrigeration business.

- The company bagged major orders in commercial refrigeration from UP Medical Supplies Corporation, Dr. Reddy’s Labs, and Thyrocare in Q2. It also launched Touchless Storage Water Coolers and Bottled Water Dispenser in Q2 which are expected to gain good traction.

- The company reached a market share of 3% in water purifiers.

- The Professional Electronics and Industrial Systems business saw revenue fall to Rs 43 Cr from Rs 89 Cr last year. The dip in revenue and profits in Q2FY21 was on account of a large, one-time order in the data security business, executed in Q2FY20.

- The segment continued to do well on the back of digitization initiatives in the BFSI sector.

Investor Conference Call Highlights

- As of September end, more than 2/3 of the job sites are available for execution.

- The inventory pressure in the RAC division has been largely eased. The management expects the recovery momentum of Q2 FY ’21 to continue in the upcoming festive season as well.

- In water purifiers, the alkaline water purifier for the immunity-boosting campaign was well accepted by the target customers.

- The management has admitted that some projects in the existing project’s book have been slow but they do not expect any cancellations. The priority of the company in this space is to get the jobs restarted so that there is the visibility of cash flows emerging from these projects.

- There wasn’t any movement in prices in the RAC space.

- Channel inventory for Blue Star is at 45-60 days currently.

- In VRF, the company is #2 in the country with a market share of 19-20%. In chillers space, it has a market share of 25-30%.

- The rise in inventory in Q1 was mainly due to business disruption and it has eased off in Q2.

- Margin profile expectation in the Segment I space is 4-4.5% while in the Segment II space, it is at 7-7.5%.

- In RACs, the market is gravitating towards a mass premium range of products. Blue Star is aiming to align to market requirements, specifically in Tier 2, 3, and 4 towns, and deliver products while retaining a range of differentiators around quality and brand image.

- The split in North & South sales is even at 30-35% of sales and the company is aiming to capture more of the North zone while maintaining leadership in the South zone.

- The company is aiming to increase the share of e-commerce in overall sales to 16-17% from the current 12-12.5%.

- It will take at least 3-4 months for the impact of the prohibition on the import of completely-built air conditioning units without refrigerants to be fully absorbed in the market.

- The company now makes almost 100% of its indoor units in-house.

- The management maintains its earlier guidance of reaching breakeven in the water purifiers business in FY21.

- The company has tapered down Capex plans for FY21 and will keep it at normal levels of Rs 90-100 Cr for F21.

- The management doesn’t see any reason for inventory management to deteriorate going forward specifically heading into the festive season.