About the Company

C E Infosystems Limited (“Map My India”) was incorporated on February 17, 1995. The company is a data and technology products and platforms company, offering proprietary digital maps as a service (“MaaS”), software as a service (“SaaS”), and platform as a service (“PaaS”). They are India’s leading provider of advanced digital maps, geospatial software, and location based IoT technologies.

Q4 FY23 Updates

Financial Results & Highlights

Detailed Results:

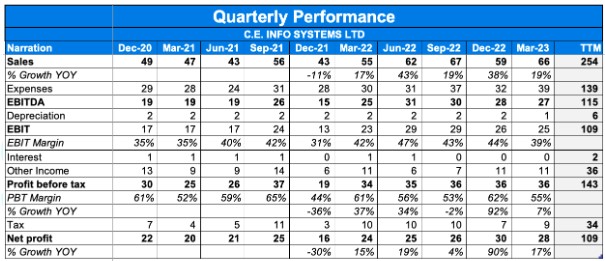

- Consolidated Total Revenue & PAT for Q4 grew by 20.7% & 25.3% respectively.

- EBITDA Margins stood at 41% in Q4FY23 which is up by 100 basis points YoY.

- Product Line Growth – Map and Data grew 27% | Platform & IoT grew 28%

- Product Line Revenue Breakup FY23 – Map and Data: 111.8 Cr | Platform & IoT: 169.7 Cr

- A&M Market grew 2.1% YoY and the C&E Market segment grew 79% YoY.

- New biz wins in C&E included:

- A multi-year extension of the contract with Big Tech company Large Marketing/Ad Agency customer upsold on Micro-Geodemographic Analytics Data Set

- 2 Large Bank & Fin-tech companies signed up for workforce & workflow monitoring, management & automation solutions

- Large F&B restaurant chain signed up for geospatial analytics for store expansion & planning

- Multiple tech-enabled companies – Used car platform, D2C meat/food delivery brand, enterprise CRM SaaS company – signed up for APIs/SDKs

- Smart City wins for a solution consisting of Drone Data Acquisition, Enterprise GIS, Integration with the Command and Control Centre, and a Digital Address System

- State Government wins for Drone Data Acquisition & processing for Large Scale Mapping, Ambulance Monitoring for Medical Emergencies, etc

- New biz wins in A&M included:

- Large, new 4-wheeler EV OEM entrant into the Indian market signed up for NCASE solution

- Large 4-wheeler OEM upsold on ADAS use case of NCASE solution

- Large 2-wheeler OEM signed up for NCASE solution

- Multiple 2-wheeler EV OEM startups signed up for NCASE solution

- Taxi Cab company signed up for a Video Telematics solution to monitor their cabs and also ensure the safety of their drivers and customers.

- The high-value goods-carrying company signed up for fleet security solution consisting of GPS + Online MDVR + ELock with multiple sensors on the same vehicle

- 1.9+ million new vehicles (4-wheelers, 2-wheelers and CVs, across ICE and EV segments), went built-in with MapmyIndia Mappls in FY23, up 46% from 1.3 million during FY22

- Multiple Go-lives in this year including the new MG Hector, Mahindra Scorpio-N & XUV400 Electric, Hero MotoCorp’s OneApp, Tork Motors, Ola Electric and more…

Investor Conference Call Highlights

- For 2023 , revenue went 41% to INR 282 Cr, while PAT went up 24% YoY to 108 Cr. Ebitda Margin for FY23 was maintained at 42%. The Map-led core business had a healthy margin of 52%.

- The management is very positive on the IoT business due to the very large capacity of the total addressable market, with on-road vehicles being 280 to 300 mn.

- For the nine months of last fiscal year, the EBITDA margin from the IoT led-business was 1%, which grew to 4% in Q4FY23, due to SaaS revenue kicking in.

- The company sold 1.9 lakh IoT devices in FY23 which was 3x of FY22, beating the automotive industry growth by growing 40% YoY.

- The management states that Q4 is weak when compared to the previous year due to the semiconductor shortage in Q3FY22, which pushed up Q4FY22 artificially.

- The company’s open order book has grown to Rs 918 Cr, up 31% from Rs. 699 Cr at the beginning of the year. This was based on annual new order bookings of INR512 crores, plus added 250 plus customers, B2B and B2B2C customers.

- The management states that not all customer acquisitions reflect in the open order book as a lot of it is subscription-based or transaction-based, where they get paid based on the consumption, so that doesn’t reflect in the open order book

- The management states that in the coming year they are incubating some potentially large yet unlocked opportunities in the space of consumer app and gadgets with Mappls App and Mappls Gadgets, which are already getting great reviews online.

- The management states that Google Maps was preloaded which resulted in the Competition Commission ruling against them, which will have a positive knock-on effect on MayMyIndia.

- The company is also additionally incubating and exploring in the drone space. It has built up the capability of full stack, providing drone hardware, drone services and also drone-based data analytics and solution. It is doing this both organically and through inorganic investment.

- The company’s excluding-Cash ROCE is 122%. While, Cash has grown from INR 381 Cr to 485 Cr.

- The management states that the Map-led business contributes majorly to the open orders, consisting of 700 Cr out of 900 Cr.

- On customer diversification, the management states that 54 customers form 80% of the company’s revenue. While earlier, it was 35 and the year before it was 25.

- The company has started work with a bunch of new EV platforms of big 4 wheeler companies to whom it is upselling ADAS and connected services.

- The company’s fixed asset investments have gone up from INR 4 Cr to INR 15 Cr in FY23, mainly due to renting out of devices to customer for a fee per month, which is lucrative then selling the device upfront sometimes.

- Out of the 250 customer additions, large majority are corporates with many automotive OEMs and strategic government organizations at center level.

- The management states that there is a 6 months to 1 year lag for the SaaS revenues to mainly come-in as they are sold mostly as a bundle with the hardware, with subscription for the first year being free.

- The management states that SaaS revenue this year of IoT, out of the INR60 crores, INR17 crores was SaaS revenue, INR42 crores is hardware.

- The management sees lots of potential for upselling into newer vehicles, as developed countries on average have 50%-60% vehicles with maps, while in India the number is at just 9% – 10%.

Analyst’s View

MapMyIndia has been executing well and has a long growth runway ahead of it in the geospatial and digital maps market. With more and more IoT devices coming into play coupled with its pay-per-use model means that a large part of its growth is yet to come. Compared to other players its one-stop-shop platform also attracts enterprises because in this case they only have to deal with one instead of several. It remains to be seen how the company will be able to grow its B2C app, field competition/loss of revenues from its existing customers like OLA who are planning to make their own maps devices & whether it will be able to grow at the current pace which the recent valuations seem to have already baked in. However, Given its strong growth prospects, it remains an interesting stock to keep track of.

Q3 FY23 Updates

Financial Results & Highlights

Detailed Results:

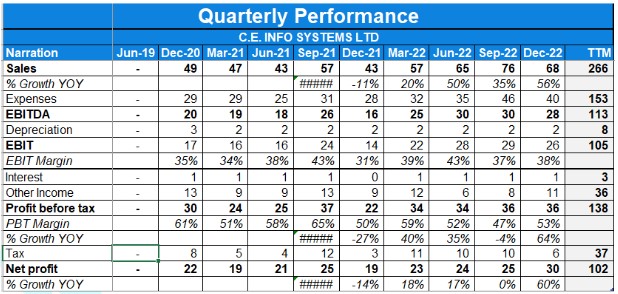

- Consolidated Total Revenue & PAT for Q3 grew by 56% & 60% respectively.

- EBITDA Margins stood at 41.1% in Q3FY23.

- Product Line Growth – Map and Data grew 51% | Platform & IoT grew 78%

- Product Line Revenue Breakup 9M – Map and Data: 164.9 Cr | Platform & IoT: 44.1 Cr

- A&M Market grew 45% YoY and the C&E Market segment grew 76.3% YoY.

- New biz wins in C&E included:

- A multi-year extension of the contract with Big Tech company Large Marketing/Ad Agency customer upsold on Micro-Geodemographic Analytics Data Set

- 2 Large Bank & Fin-tech companies signed up for workforce & workflow monitoring, management & automation solutions

- Large F&B restaurant chain signed up for geospatial analytics for store expansion & planning

- Multiple tech-enabled companies – Used car platform, D2C meat/food delivery brand, enterprise CRM SaaS company – signed up for APIs/SDKs

- Smart City wins for a solution consisting of Drone Data Acquisition, Enterprise GIS, Integration with the Command and Control Centre, and a Digital Address System

- State Government wins for Drone Data Acquisition & processing for Large Scale Mapping, Ambulance Monitoring for Medical Emergencies, etc

- New biz wins in A&M included:

- Large, new 4-wheeler EV OEM entrant into the Indian market signed up for NCASE solution

- Large 4-wheeler OEM upsold on ADAS use case of NCASE solution

- Large 2-wheeler OEM signed up for NCASE solution

- Multiple 2-wheeler EV OEM startups signed up for NCASE solution

- Taxi Cab company signed up for a Video Telematics solution to monitor their cabs and also ensure the safety of their drivers and customers.

- The high-value goods-carrying company signed up for fleet security solution consisting of GPS + Online MDVR + ELock with multiple sensors on the same vehicle

Investor Conference Call Highlights

- The effective tax rate was lower than 25% in Q3, due to the reason of nil tax on the unrealized gain of Rs. 4.23 crores towards the revaluation of investments carried at fair market value under the head of other income coupled with the lesser rate of tax applicable on capital gains than on business income.

- The management explains that the high growth in the IoT business compresses margins initially, as device hardware has lower margins, but starts creating high-margin SaaS revenue in the future, typically 12 months down the road.

- Out of the total 44.1Crs of revenue from the IOT biz, the sale of Map data and services including royalty, annuity, software, and projects called MaaS, PaaS, SaaS, and subscription contributed Rs. 12.4 crores.

- Margins were aided by lower marketing expenses.

- The sales for the company have outperformed the automotive OEM industry volume growth.

- The new products introduced include the core foundation map, Geo analytics data set, the 3D Metaverse, 360-degree real view maps, HD maps such as NCASE for automotive digital transformation platform, APIs and SDKs, Geospatial Platform, and drone-based solutions.

- The company is increasing its focus on consumer B2C apps.

- The management explains the seasonality where Q1 and Q3 are typically lower than Q2 and Q4.

- The company invested up to Rs. 7 crores for a 20% stake in a drone company called Indrones this company because it requires drones for its own mapping activities, it’s synergistic with the overall offering of geospatial and IoT also help offer various solutions to various set of customers.

- Google has received orders against anti-competitive practices & is unable to get relief in any court. The management will shape its biz strategy for the B2C app post clarity on the situation.

- OLA is still using the company’s maps & management believes this is unlikely to change as it’s difficult for any company (including Ola which recently acquired a stake in mapping co.) to build its own map system.

- The measurement criteria for its investments is the lower of the latest valuations at which funding was raised & the fair market valuation report it receives.

- The dividend policy depends on A) cash needed for its portfolio investments, B) additional investment opportunities in the areas related to its business & C) normal & safe requirements for the business of the company.

Analyst’s View

MapMyIndia has been executing well and has a long growth runway ahead of it in the geospatial and digital maps market. With more and more IoT devices coming into play coupled with its pay-per-use model means that a large part of its growth is yet to come. Compared to other players its one-stop-shop platform also attracts enterprises because in this case they only have to deal with one instead of several. It remains to be seen how the company will be able to grow its B2C app,field competition/loss of revenues from its existing customers like OLA who are planning to make their own maps devices & whether it will be able to grow at the current pace which the recent valuations seem to have already baked in. However, Given its strong growth prospects, it remains an interesting stock to keep track of.

Q2 FY23 Updates

Financial Results & Highlights

Detailed Results:

- Consolidated Total Revenue & PAT for H1 grew by 41% & 8% respectively..

- EBITDA Margins stood at 40.1% in Q2FY23. Ebitda margins for H1 were 42.8%.

- Cash and Cash Equivalents stand at Rs. 430.6 cr.

- Product Line growth – Map and Data grew 32% | Platform & IoT grew 49%

- Product Line Revenue Breakup – Map and Data: 59.4 Cr | Platform & IoT: 81.9 Cr

- A&M Market grew 55% YoY and C&E Market segment grew 29% YoY

- Business Update – New additions

- • New large 4-wheeler EV OEM signed up

- • Market-leading vehicles from leading brands continue to go live embedded with our solutions

- Multiple large cement and dairy companies signed up for using IoT & Logistics SaaS solutions

- • Multiple BFSI/fin-tech companies for Workforce management & automation

- • E-commerce, FMCG and fin-tech companies for Geospatial Analytics

- • Health-tech, fin-tech, retail/FMCG & voice-assistant app developers for APIs

Investor Conference Call Highlights

- The company acquired a 76% stake in Gtropy, An IOT-based company which will help the company to tap a vast market of 20 Crs plus vehicles in an accelerated manner.

- EBIDTA of core biz remained at 50%, but the acquisition led to EBIDTA declining to 42.8% on a consolidated basis.

- Other reasons for margin declines include higher marketing expenses & investments in product developments like Realview 360-degree and Metaverse 3D maps.

- The company also invested INR 10 crores for a 26% stake in a company Kogo, a gamified social travel commerce platform, which will open up new markets and new use cases.

- PAT margins were negatively affected due to lower other income & higher effective tax rates.

- The company in coming years targets EBIDTA margins of not less than 40%.

- The company A&M revenues excluding Gtropy grew by around 40% which is in line with the PV industry’s growth.

- API’s contribution to C&E stood at around 50%.

- The 3 components of Gtropy biz are pure device, pure Saas & device-led SAAS.

- The management is targeting a strategy of providing devices to its B2B customers like cement & dairy cos at lower margins & then generating recurring high-margin revenues through Saas offering.

- The management explains that Gtropy gets the benefit of the muscle power of Mapmyindia to extend its offering widely & the company gets the benefit of Gtropy by neutralizing the shortfall in its IoT revenues.

- The company’s end objective of working with Govt. is to be part of population-scale platforms since, the government has big plans for digital transformation, Geospatial and IoT, and maps, the areas where the company can play a critical role.

- The company’s tie-ups with Govt. include the ULIP project, which is the Unified Logistics Interface Platform government announced with National Logistics Policy & partnership with U.P. police.

- The company is not seeing any slowdown in E-commerce & Fintech space in the C&E segment.

- The management states that the majority of EV two-wheelers are looking at its NCASE product.

- The management explains that the auto OEM business is mostly a volume-based business while the fixed price normally comes in the C&E side and is use case driven.

- The Gtropy’s revenues doubled QoQ to Rs.24 Crs out of which Rs.8 Crs was attributable to a Saas offering made to Mapmyindia.

- The management believes that the company is unique Vs its global peers due to its highly technology-oriented and cost-efficient strategy.

- The company’s framework while evaluating an acquisition is whether it will get us more customers they will enhance the product portfolio or that it can upsell to its existing customers.

- The company plans to monetize its KOGO acquisition by continuing to sell to its OEM customers as add-on solutions & direct-to-consumers monetization opportunities.

- The management on being asked about a potential advertising-led business model commented “t I don’t want to preclude anything for the long-term future. What we are strong procurement of, is user privacy. We don’t believe in this ad user targeting and mining, that’s the Google route, which we are not a fan of.”

Analyst’s View

MapMyIndia has been executing well and has a long growth runway ahead of it in geospatial and digital maps market. With more and more IoT devices coming into play coupled with its pay-per-use model means that a large part of its growth is yet to come. Gtropy acquisition is likely to provide it a good headstart in the owned and logistic fleet device market. Even on the Government side, while the revenue share last year was 5%, management expects growth in this segment as well. Compared to other players its one-stop-shop platform also attracts enterprises because in this case they only have to deal with one instead of several. A cash balance of nearly Rs. 400cr provides it with enough M&A dry powder to scout and grab any suitable opportunity.Given its strong growth prospects, it remains an interesting stock to keep track of.

Q4 FY22 Updates

Financial Results & Highlights

| Standalone Financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 66.6 | 55.9 | 19.1% | 49.3 | 35.1% | 237.1 | 192.1 | 23.4% |

| PBT | 33.9 | 24.7 | 37.2% | 19 | 78.4% | 115 | 79 | 45.6% |

| PAT | 23.5 | 20.4 | 15.2% | 15.7 | 49.7% | 85.5 | 60.1 | 42.3% |

| Consolidated Financials (in Crs) | ||||||||

| Q4FY22 | Q4FY21 | YoY % | Q3FY22 | QoQ % | FY22 | FY21 | YoY% | |

| Sales | 68.6 | 56 | 22.5% | 52 | 31.9% | 242 | 192.2 | 25.9% |

| PBT | 33.5 | 24 | 39.6% | 21.7 | 54.4% | 117 | 78.8 | 48.5% |

| PAT | 22.5 | 19 | 18.4% | 18.5 | 21.6% | 87 | 59.8 | 45.5% |

Detailed Results:

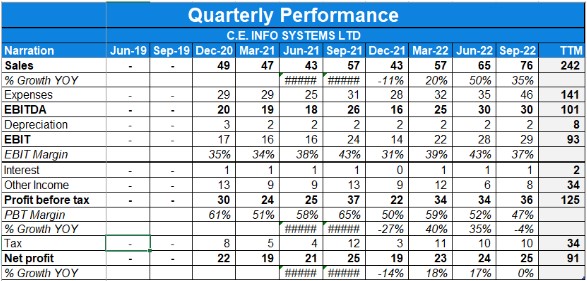

- The company had a decent quarter with a 22% YoY rise in consolidated revenues and a 18% YoY rise in consolidated PAT.

- FY22 revenues were up 26% YoY and PAT was up 45.5% YoY.

- EBITDA margins for FY22 expanded to 43% from 35% the previous year. PAT margins expanded to 36% from 31% the previous year.

- The cash and cash equivalents of the company stand at 382 Cr.

- In Market Segment, A&M revenue has grown 41% YoY for FY22. C&E revenue has grown 21% YoY for FY22.

- In Product Segment, revenue from Map & Data is up 37% YoY. Platform and IoT revenue grew 28% YoY for FY22.

- The company’s Open Order Book as of April 1, 2022, stood at Rs. 699.6 Crores vs Rs 377.5 Cr as of April 1, 2021.

- The No. of Customers on MaaS, SaaS & PaaS platforms in FY22 grew by more than 100 to 600+ customers.

- New deal wins in A&M segment for Q4FY22 included :

- Indian Motorcycle OEM signed up and went live

- Indian EV 2-Wheeler OEM startup signed up

- Japanese Mobility as a Service provider signed up

- Largest 4-wheeler OEM went live with their next-gen connected vehicles integrated with the company’s maps & technologies

- Nissan partnered for Road Safety initiative by using the company’s Road Safety Platform

- New deal wins in C&E segment included :

- 2 Large FMCG majors went live with geospatial analytics and workforce automation use cases respectively

- Large E-commerce company signed up for geospatial analytics

- Large CRM SaaS company signed up for integrating map APIs for providing their customers with in-built location intelligence

- Large Global Social Media App integrated map data to provide a better location-based end consumer experience in India

- A Smart City signed up for GIS-based Property Tax Solutions

- State Urban Development Authority signed up for Drone and 3D mapping-based GIS System with multiple end use cases

- Large Safe City in South India signed up for Crime Mapping & Analytics

- Large State Road Transport Corporation signed up for Public Transport Platform

Investor Conference Call Highlights

- The company’s R&D expenses were approximately Rs.3 Cr in FY21 which increased to Rs.5 Cr in FY22.

- The management states that there are five growth engines to its automotive business – selling navigation systems, connected systems, ADAS, autonomous systems, shared mobility as well as an electric mobility system.

- The company acquired a 76% stake in Gtropy to give a specific focus on the IoT and logistic SaaS part of its business.

- 1.3 million new vehicles in FY22 were integrated with the company’s maps & technologies vs 1 million new vehicles in FY21.

- The company’s 35 customers contributed 80% of its total revenue while 92% of the large customers were retained in FY22.

- The number of employees increased in FY22 to 936 from 734 YoY.

- The attrition rate increased from 13.5% to 17.45% YoY.

- The Govt contribution in the current mix is 10% & the management has put an upper cap limit of 20% on that.

- The company launched Maapls to service the global market.

- The management expects to spend 2-3% of revenue on R&D which majorly constitutes the cost of people employed in the R&D segment.

- The management expects the EBIDTA margin to be in the range of 35-43%.

- The employee costs were lower by Rs.5 Cr in Q4 due to the reversal of a provision created for employee incentives & bonuses.

Analyst’s View

C E Infosystems (MapMyIndia) is a leading provider of advanced digital maps, geospatial maps, and location-based IoT technologies. Its business is seasonal with heavy revenue being booked in the latter half of the year due to the nature of its revenue recognition and contracts. Its customers include the government and big companies giving it recurring revenue. The management is highly positive about the company’s future. The company has done well to bag multiple orders for it’s A&M and C&E segments. It has also acquired Gtropy which should help them expand well in the industrial IoT segment. Recent changes in government policies that worked in favor of the company give a positive roadmap to the company. Huge market opportunities in digital maps and geospatial data give huge growth potential to the company. Yet, current valuations offer no margin of safety for a value investor. Nonetheless, being a one-of-its-kind company in its niche industry, C E Infosystems is a company that should be under every investor’s watchlist.

Q3 FY22 Updates

Financial Results & Highlights

| Standalone Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2Y22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 49 | 61 | -19.6% | 69 | -28.9% | 171 | 136 | 25.7% |

| PBT | 19 | 29 | -34.4% | 36 | -47.2% | 81 | 54 | 50% |

| PAT | 15 | 22 | -31.8% | 25 | -40% | 62 | 39 | 58.9% |

| Consolidated Financials (In Crs) | ||||||||

| Q3FY22 | Q3FY21 | YoY % | Q2FY22 | QoQ % | 9MFY22 | 9MFY21 | YoY% | |

| Sales | 52 | 61 | -14.7% | 70 | -25.7% | 174 | 136 | 27.9% |

| PBT | 21 | 29 | -27.5% | 37 | -43.2% | 84 | 54 | 55.5% |

| PAT | 18 | 21 | -14.2% | 25 | -28% | 65 | 40 | 62.5% |

Detailed Results:

- The company had a bad quarter with a -14.7% YoY fall in consolidated revenues and a -14.2% YoY fall in consolidated PAT.

- 9M revenues were up 27.9% YoY and PAT was up 62.5% YoY.

- Company has currently 500+ customers on SaaS, PaaS and MaaS platforms.

- The company recently listed last quarter and was subscribed 155 times, listing at a 53% premium.

- EBITDA margins on 9M basis expanded 44% from 32% the previous year. PAT margins expanded to 37% from 30% the previous year.

- The cash and cash equivalents of the company stand at 389.6 Cr.

- Sales of automotive OEMs were impacted due to semiconductor shortage which in-turn affected the company.

- In Market Segment, A&M revenue has grown 39.5% YoY for 9M. C&E revenue has grown 33.3% YoY for 9M.

- In Product Segment, revenue from Map & Data is up 25.1% YoY. Platform and IoT revenue grew 44.1% YoY for 9M.

- Ministry of Road Transport and Highways signed an MoU with MapMyIndia for integrating information of accident-prone road stretches and promoting MapMyIndia’s app, that gives real-time ADAS safety alerts to drivers during navigation, to users across India.

- QSR company’s adopted MapMyIndia for evaluating and selecting restaurant sites based on MapMyIndia’s geospatial data and analytics platform.

- The board gave approval for acquiring 9.99% stake in, Pupilmesh Pvt Ltd, a young, exciting automotive tech and augmented reality metaverse tech company, for a consideration of Rs. 49.95 lakhs.

- Government health agency selected MapMyIndia to power GIS (Geospatial Information Systems) and location based services for India’s health services.

Investor Conference Call Highlights

- The company signs long term mutually renewable contracts of three to five years with its customers to whom they provide platforms, APIs, etc. and charge fees per period.

- The management states that the addressable market for the company’s area is set to grow to $4.2 Billion for digital map services and $44 billion for navigation solutions and telematics by the year 2025.

- The management states that the company’s business model is such that it is best understood when numbers are compared YoY.

- The management expects quarterly revenues to get normalized and covered up as supply chains recover.

- Some of the B2B and B2B2C contracts that the company receives are milestone-based due to which revenues get recognized in certain timeframes resulting in lumpy revenues.

- The management is confident about the next quarter’s for the company.

- One of the leading European four-wheeler OEMs went live with MapMyIndia for in-vehicle navigation in Q3.

- Bajaj Finance super app went live with MapMyIndia to power their consumer facing mapping services and for location enabling their digital transformation across their enterprise operations.

- A publicly listed QSR company adopted MapMyIndia geospatial data analytic platform.

- The management states that 35% – 40% range for PAT margin is sustainable for coming years ahead.

- The ESOP charges for the quarter have been 92 lakhs.

- The company’s order book materializes at an average of 3.5 years.

- Geospatial guidelines released by the government give an advantage to the company by restricting foreign entities from doing a vehicle-based ground survey and terrestrial mobile mapping survey.

- The company has good direct business with the government, with the government to 20% of its business.

- The acquisition of stake in Pupilmesh Ltd was to ride the wave of Metaverse and AR.

- Pupilmesh is currently working on a helmet for two-wheeler riders to help in navigation and reduce accidents.

- The company’s addressable market for navigation solutions and telematics is $44 Billion by 2025.

- While the platforms already exist, the company will spend going forward into investments and improvements in technology.

- The management admits about the seasonality existing in the business with Q4 of the year having heavy revenues because of the terms of some contracts.

- MapMyIndia in comparison to google has better precision, accuracy and flexible pricings therefore making it more preferred to customers.

Analyst’s View

C E Infosystems (MapMyIndia) is a leading provider of advanced digital maps, geospatial maps and location-based IoT technologies. Its business is seasonal with heavy revenue being booked in the latter half of the year due to the nature of its revenue recognition and contracts. Its customers include the government and big companies giving it recurring revenue. The management is highly positive about the company’s future. Recent changes in government policies which worked in favour of the company give a positive roadmap to the company. Huge market opportunities in digital maps and geospatial data give huge growth potential to the company. Yet, current valuations offer no margin of safety for a value investor. Nonetheless, being a one-of-its-kind company in its niched industry, C E Infosystems is definitely a company that should be under every investors watchlist.

Disclaimer

This is not an investment advice. Please read our terms and conditions.