When most businesses in India are focused on surviving Covid-19, it is a good time to invert the situation and think about companies that are still managing to proceed with their CapEx plans.

Companies that can invest in CapEx today get better bargains as prices are depressed due to low economic activity, creating a sustainable advantage for them over time.

Investopedia defines Capex as follows:

Capital expenditures, commonly known as CapEx, are funds used by a company to acquire, upgrade, and maintain physical assets such as property, buildings, an industrial plant, technology, or equipment. CapEx is often used to undertake new projects or investments by the firm. Making capital expenditures on fixed assets can include everything from repairing a roof to building, to purchasing a piece of equipment, to building a brand new factory. This type of financial outlay is also made by companies to maintain or increase the scope of their operations. Put differently, CapEx is any type of expense that a company capitalizes, or shows on its balance sheet as an investment, rather than on its income statement as an expenditure.

I am not going to go into the formulae and calculations as those are available on the internet. The focus of this post is rather to go beyond the formulae and think on these lines:

- Balance Sheet Strength of a company – A Strong Balance Sheet can fund CapEx even in times of economic crises such as the COVID-19 pandemic. However, when the Balance Sheet is not robust, the management will have to either delay CapEx or take up debt to fund it. As an investor, to gauge the strength of the Balance Sheet, you have to look for financial metrics like debt levels, working capital cycle, interest coverage ratio, and so on so forth.

- Management’s willingness to invest: Having Balance Sheet strength is not enough. The management must be willing to invest the cash into potential growth propositions. And you will not find this information in the Annual Reports. You have to check management’s recent commentaries on the recent quarterly result conference call, or in a recent interview to financial media. When they respond to the questions on capital allocation, you get a fair idea as to how they are positioning themselves to face any crisis.

After thinking for a while, I came up with this framework:

For each quadrant, an investor can think in the following way:

- Quadrant 1 (Less Focus): Should wait for an attractive valuation to buy these companies for two reasons. Either they are not capitalizing on opportunities or their industry conditions do not allow them to invest aggressively in CapEx. Hence, they will have a potentially lower growth trajectory. Hence as investors, we should focus less on these companies.

- Quadrant 2 (No Focus): These companies are disadvantaged on both fronts. Whatever be the valuation or industry standing, these companies should not be in the portfolio at the current juncture. They can only be looked at if at least one of the aspects (Balance Sheet strength or management’s willingness to commit CapEx) show improvement. So, we should not focus on these companies from a portfolio point of view irrespective of their valuation.

- Quadrant 3 (Selective Focus): Should be bought only at compelling valuations to offset the risk associated with these businesses and their leveraged Balance Sheet. Hence, we should be very selective in this space. Some companies may surprise positively while many may disappoint due to the inherent risk associated with a high-debt company.

- Quadrant 4 (More Focus): Be ready to pay-up (but not overpay) for these businesses as they will see faster growth in earnings compared to all other businesses. This where an investor should focus most.

SUBSCRIBE to our mailing list

- For better understanding, we can look at a few stocks from the Sensex and try to figure out which quadrant of the above framework they fit into.For the sake of simplicity, we will exclude the financial companies for the above framework as their business model is different. For financial companies, cash is their raw material, and bulk of their funds’ requirement is for providing loans and maintaining the statutory liquidity requirement imposed by the RBI. CapEx is not a significant consideration for them.So, if we remove the eight finance companies from the list of companies in Sensex, we are left with the following 22 companies:

Reliance Maruti Suzuki Ultratech Cement M&M TCS Asian Paints ONGC Tech Mahindra HUL Nestle NTPC Hero Motorcorp Bharti Airtel HCL Technologies Power Grid Tata Steel Infosys L&T Titan ITC Sun Pharma Bajaj Auto

If we analyze the Balance Sheet and the management commentary at the current juncture for the above companies, we can place them like this:

Now, I am not recommending to buy and sell based solely on the above quadrants. Investing is not that easy.

This framework is just a starting point. It only takes into account two aspects:

- Balance Sheet Strength

- Capital Allocation policy

Before buying a stock one must look into several other factors like industry situations, the company’s position in the industry, valuation of the stock, earnings growth prospects, and so on and so forth.

But having this framework in mind may help an investor make a more informed decision.

And some of the most attractive investments happen when you can spot a business which moves in one of the following ways:

| Direction of Movement | Reasons |

| Q2-Q3-Q4 | The company aggressively invests in CapEx by taking debt on books, improves Cash Flows, and then pay off debt over a period of time while continuing to invest in CapEx to grow. |

| Q2-Q1-Q4 | The company first improves its financial position. The cash flow of the company starts growing steadily. And then the company starts investing in CapEx for future growth. |

| Q1-Q4 | The company already has the financial muscle-power. It starts using that power by investing in the right opportunities for growth. |

| Q3-Q4 | By investing in CapEx and growing fast, the company improves its finances over time. |

Now, it’s time to take a look at one company that moved from Q3 to Q4 in a few years and generated wealth for its shareholders.

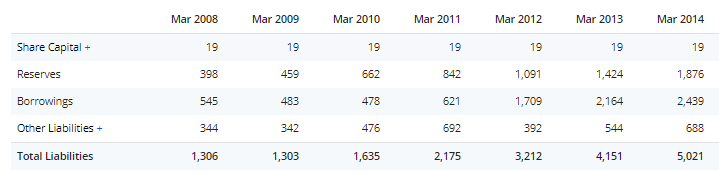

Look in the above chart, how debt has consistently increased from less than 500 Cr in 2010 to about 2439 Cr.

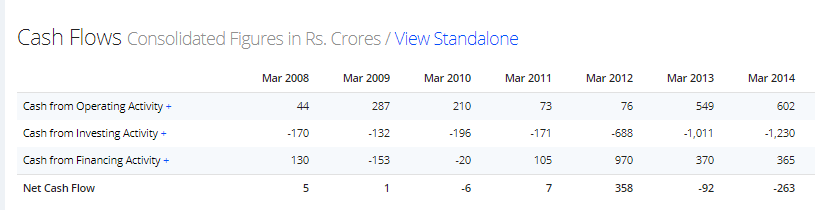

And during the same period, they kept on investing heavily in CapEx as you can see above. From less than 200 Cr of annual CapEx until 2011, the company did around 3000 Cr of CapEx in the next three years.

And the stock of this company was trading in the range of 6 times to 12 times earnings from FY11 to FY14.

And do you know what happened in the years after FY14?

Look closely at the Reserves and Borrowings from FY15 onwards.

As the company started reaping the benefit of massive CapEx done until FY14, in the years that followed, the Reserves (or the Equity) kept going up and debt started coming down.

And the result of this was captured in the price as well.

It is now time to reveal the name of the company.

You would have probably guessed it by now.

Yes, it is Balkrishna Industries. You may like to read more about it here.

So, next time when you analyze a business, try to decipher, in which quadrant it falls into. And also try to understand in which quadrant it can go to in the near future.

This framework will not only save you from Landmines but also help you find the Dark Horses.

Happy investing!

Disclaimer

This is not investment advice. Please read our terms and conditions.