A few days back I was chatting with my friend Anshul and he asked me something interesting.

“Ankit, many stocks have corrected in past 6-8 months. Some reports say that average fall across 3,000 traded stocks is more than 50% from their 2018 Highs. Which has resulted in quite a few popular names which used to be market darlings being available at relatively cheaper valuations. For example, Eicher Motors is down by 40% from its all time high. Rain Industries — the most talked about 10-bagger of 2018 — has fallen by 75% in last one year.” Anshul said.

“Right, Anshul.” I nodded.

However, the Nifty hasn’t corrected that much, added Anshul, “It’s is barely down 10% from its lifetime high. Which means several of the blue chip companies are still doing well in terms of returns to the shareholders in past few years. And most of these large caps have been around for a long time and they have proven and profitable business models. For example, companies like HDFC Bank, Asian Paints, TCS, etc.”

“Yes. So what’s your point?” I asked him.

“For many of these names, there’s little doubt about the quality of the business or future potential, then what stops you from buying them at this stage?” Anshul asked.

Anshul’s question got me thinking. I am sure this question is also on the minds of many of our blog readers and even several of our clients. So I thought it would be best to compile my thoughts in form of a post.

The current situation reminds me of Warren Buffett’s famous quote —

What the wise do in the beginning, fools do in the end.

In the stock market, there’s no dearth of examples of outstanding companies which were a drag to the portfolio of investors. And in most such cases, it wasn’t necessarily because those companies did not grow their earnings beyond a point, but more so because the market participants had set an obscenely high expectation of their future performance. A few wise (or may be lucky) investors could identify those stocks early and ride the wave and then eventually those stocks become the darlings of the stock market. We all fall for the story in the stock and we forget about the basic principle of investing: “Margin of Safety.”

Holding stocks for the long term is by far the best way of compounding wealth. However, before holding them, we have to buy them. Buying stocks cannot be based on our whims and fancies. It has to follow a process with clear attention to —

1. Industry

2. Business

3. Management

4. Price/Valuation

We may choose to hold shares of a good quality company at a temporary elevated valuation only if we bought it at reasonable valuations. However, buying companies at unrealistic valuations always creates the risk of sustained under-performance of the portfolio.

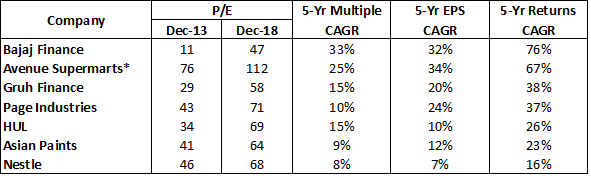

I recently came across this study by 2point2 capital (a SEBI registered PMS). Click here if you can’t see the image below.

There is no doubt that all these companies are outstanding businesses with impeccable management thriving in industries which have a lot of tailwind. However, a closer look reveals that the market has rewarded these companies with a return which exceeds their earnings growth by a big margin. There is a case where some of the above companies may go on to do well for a long run and earnings might catch up the valuations along the way. However, betting on these at this juncture appears to me as playing with fire.

In fact, another of Buffett’s saying fits well in current situation. He said —

In the business world, the rear-view mirror is always clearer than the windshield.

When the party is over, we will have experts pointing out the point at which buying these stocks were unfathomable. Investing is hard. Staying away from these stocks even when they rise daily, is not a happy feeling for an investor. However, the principles of investment teaches us that we have to play this hard game with due diligence and focus on the process.

While investing is all about embracing uncertainty, we must not forget to ask ourselves — At What Cost?

At this point you may be tempted to remind me of this quote from Charlie Munger (Warren Buffett’s long time business partner) —

Over the long-term, it’s hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you’re not going to make much different than a 6% return even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive looking price, you’ll end up with a fine result.

There’s nothing wrong in Munger’s argument. However, it’s dangerous to read the quote with an intention to rationalize the investments in overvalued stocks, which many long term investors often do.

If an investor is willing to hold a high PE stock for next 20 years and hopes that the business continues to return 15-18% on capital, isn’t it going to turn out well in the end? What’s wrong in this line of reasoning?

My short answer to this argument is this — very low margin of safety.

The long answer —

A stock runs up in the long run on the basis of 3 primary reasons

a. Growth in earnings, or

b. Growth in multiple, or

c. Combination of both a&b

Future, as we all know is unpredictable. Earnings may or may not rise as we expect. Valuation multiples may or may not grow as we expect. To increase our odds of making a profitable investment, it is hence advisable to have a margin of safety.

If you buy an outstanding company’s stock at high valuations the only way for you to make money is that the company keeps growing its earning at a very high rate. And this stellar performance has to continue year on year for a long time.

Now, take a look at all the companies around. How many of them have given a consistent stellar performance year on year for a long time? Only a handful. Even in case of these companies, it is not a sure bet that they will continue to grow as they did in the past.

Hence the only way to be prepared for an uncertain future is to buy outstanding businesses at reasonable valuations (if not low).

I hope my rationale gives you some respite from the strong sense of FOMO (fear of missing out) which is prevailing these days in the stock market.